Insights from recent episode analysis

Audience Interest

Podcast Focus

Publishing Consistency

Platform Reach

Insights are generated by CastFox AI using publicly available data, episode content, and proprietary models.

Total monthly reach

Estimated from 2 chart positions in 2 markets.

By chart position

- 🇳🇿NZ · Investing#111500 to 3K

- 🇭🇰HK · Investing#165500 to 3K

- Per-Episode Audience

Est. listeners per new episode within ~30 days

300 to 1.8K🎙 Daily cadence·195 episodes·Last published today - Monthly Reach

Unique listeners across all episodes (30 days)

1K to 6K🇳🇿50%🇭🇰50% - Active Followers

Loyal subscribers who consistently listen

550 to 3.3K

Market Insights

Platform Distribution

Reach across major podcast platforms, updated hourly

Total Followers

—

Total Plays

—

Total Reviews

—

* Data sourced directly from platform APIs and aggregated hourly across all major podcast directories.

On the show

Recent episodes

Unisys: From UNIVAC to the Cloud — A Mainframe Giant's Survival Story - $UIS

May 16, 2026

Unknown duration

$HNI: The Office Furniture Powerhouse You've Never Heard Of

May 15, 2026

Unknown duration

Centrus Energy: The Last American in the Room - $LEU

May 14, 2026

Unknown duration

Keros Therapeutics: The Biology-First Bet on TGF-Beta Superfamily - $KROS

May 13, 2026

Unknown duration

MARA Holdings: From Penny Stock to Bitcoin's Bellwether - $MARA

May 12, 2026

Unknown duration

Social Links & Contact

Official channels & resources

Official Website

Login

RSS Feed

Login

| Date | Episode | Description | Length | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 5/16/26 |  Unisys: From UNIVAC to the Cloud — A Mainframe Giant's Survival Story - $UIS | How does a foundational technology pioneer survive four decades after its core business becomes obsolete? The story of Unisys Corporation is a captivating masterclass in the art of corporate survival, tracing its lineage from the legendary UNIVAC machine that stunned America by predicting the 1952 presidential election to its modern existence as a struggling, yet stubbornly resilient, IT services underdog. Riddled with one of the industry's most disastrous mergers, crushing pension crises, and multiple near-death encounters with bankruptcy, Unisys has repeatedly defied the grave by leveraging sticky government contracts and the inescapable switching costs of legacy mainframes. Dive into this fascinating saga to discover how a former titan navigated the ruthless innovator's dilemma, orchestrated high-stakes pivots into cloud and cybersecurity, and ultimately blurred the line between truly succeeding and simply refusing to die.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/UISI. Introduction & Episode RoadmapII. The UNIVAC Legacy and Computing's First ActIII. The Burroughs-Sperry Merger: "Synergy" Gone Wrong (1986)IV. The Lost Decade: Near-Death and Debt Crisis (1990–2003)V. The Weinbach Turnaround: Stabilization (1997–2008)VI. The Second Near-Death Experience (2008–2012)VII. The Altabef Era: Reinvention or Just Survival? (2014–Present)VIII. The Business Model EvolutionIX. Culture, Leadership, and the Survival MentalityX. Competitive Analysis: Porter's Five Forces and Hamilton's Seven PowersXI. Bull vs. Bear CaseXII. Key Inflection Points SummaryXIII. Lessons for Founders, Operators, and InvestorsXIV. The Future: What Happens Next?XV. Epilogue and Final ReflectionsXVI. Further Reading and Resources | — | ||||||

| 5/15/26 |  $HNI: The Office Furniture Powerhouse You've Never Heard Of | Imagine sitting in a typical American corporate office; there is a staggering chance that the desk, chair, or filing cabinet you are using was built by a company you have never heard of. Meet HNI Corporation, a scrappy Iowa manufacturer that quietly conquered the office furniture industry not with flashy designs, but through a relentless, almost fanatical devotion to operational efficiency, a unique "member-owner" culture, and a shrewd roll-up acquisition strategy that recently culminated in the multi-billion-dollar takeovers of Kimball International and Steelcase. As the post-pandemic era ushers in hybrid work and "resimercial" aesthetics, this invisible giant now faces its ultimate test: adapting its unmatched manufacturing machine to a world where the very purpose of the physical office is being fiercely debated. Dive into the fascinating eight-decade history of how a $4,000 investment birthed a $6 billion powerhouse, and discover whether HNI's quiet competence is enough to secure its dominance in the unpredictable future of work.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/HNII. Introduction and Episode RoadmapII. The Member-Owned Foundation: Understanding HNI's Unusual DNAIII. From Kitchens to Cubicles: The Office Furniture Pivot (1960s-1980s)IV. The Roll-Up Era: Acquiring the "Good Enough" Brands (1990s-2000s)V. The Great Recession and Structural Challenges (2008-2015)VI. The Quiet Transformation: E-Commerce and Supply Chain Mastery (2010s)VII. The Pandemic Inflection Point: COVID-19 and Work-From-Home (2020-2021)VIII. The Return-to-Office Reckoning (2021-2024)IX. Portfolio Strategy and Brand Architecture TodayX. The Current Playbook: How HNI Competes TodayXI. The Steelcase Gambit and Porter's Five ForcesXII. Bull vs. Bear CaseXIII. What to Watch: KPIs and Future SignalsXIV. Epilogue: The Quiet Giant's Next ChapterXV. Resources for Further Research | — | ||||||

| 5/14/26 |  Centrus Energy: The Last American in the Room - $LEU | From the secretive origins of the Manhattan Project to the brink of corporate collapse, the story of Centrus Energy Corp reads less like a standard financial analysis and more like a high-stakes geopolitical thriller. As the only company capable of enriching uranium using American-origin technology, Centrus miraculously survived decades of cheap Russian fuel dependence to emerge as the indispensable linchpin of today's nuclear renaissance. With the artificial intelligence boom driving unprecedented electricity demand and Western nations urgently severing their reliance on adversarial supply chains, Centrus now holds the exclusive keys to producing HALEU—the specialized fuel required to power the world’s next-generation reactors. Dive into this fascinating saga to discover how a forgotten Cold War relic transformed into America's most strategically vital energy asset, and explore the massive technological and financial hurdles that still stand between its bold promise and operational reality.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/LEUI. Introduction and Episode RoadmapII. Origins: The Manhattan Project to USECIII. The Russian Shadow: Megatons to MegawattsIV. Technology Crisis: The American Centrifuge GambleV. Near-Death Experience: Bankruptcy and RebirthVI. Geopolitical Inflection: Russia, China, and Energy SecurityVII. The HALEU Breakthrough: Becoming Essential AgainVIII. Recent Developments: The 2024-2025 InflectionIX. The Nuclear Renaissance and AI Data Center BoomX. Business Model and Strategy: From Death to Dominance?XI. Competitive Landscape and Industry StructureXII. Strategic Analysis: Porter's Five ForcesXIII. Strategic Analysis: Hamilton Helmer's Seven PowersXIV. What Could Go Wrong? And What Could Go Right?XV. Lessons and ReflectionsXVI. Where Are They Now and What Is NextXVII. Final ReflectionsXVIII. Key Takeaways and Further LearningXIX. Further Reading and Resources | — | ||||||

| 5/13/26 |  Keros Therapeutics: The Biology-First Bet on TGF-Beta Superfamily - $KROS | Dive into the high-stakes, rollercoaster world of clinical-stage biotech through the captivating story of Keros Therapeutics. Founded by a visionary scientist who walked away from a multi-billion-dollar success to build a "better engine" for targeting the body's complex TGF-beta master switches, Keros embodies the extreme risks and profound rewards of modern drug development. In just a few years, the company has weathered a pandemic-era IPO boom, celebrated breakthrough clinical data, secured a massive global partnership with Takeda, and survived a devastating pipeline failure that slashed its workforce and forced a dramatic strategic pivot. With the company's future now hinging on a pivotal Phase 3 trial for a potentially life-changing blood disorder therapy, this deep dive explores the underlying molecular science, the boardroom dealmaking, and the very real human lives hanging in the balance—offering a gripping look at what it truly takes to bring a next-generation medicine to the world.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/KROSI. Introduction and Episode RoadmapII. The Scientific Foundation: Why TGF-Beta MattersIII. Founding Story and the Pontifax Connection (2015-2017)IV. Building the Pipeline: The Platform Strategy (2017-2019)V. The IPO and Going Public (April 2020)VI. Clinical Inflection Point No. 1: KER-050 Phase 2 Data (2021-2022)VII. Clinical Inflection Point No. 2: Expanding to Myelofibrosis (2022-2024)VIII. The Licensing Deals: From Hansoh to Takeda (2021-2025)IX. The Cibotercept Crisis and Corporate Restructuring (2024-2025)X. KER-065, the Pivot to Neuromuscular Disease, and the Phase 3 in MDS (2024-2026)XI. The Competitive Landscape and Strategic PositioningXII. Company Culture and Execution PlaybookXIII. Porter's Five Forces and Hamilton's 7 Powers AnalysisXIV. Bull vs. Bear CaseXV. The Narrative Arc and LessonsXVI. Epilogue: The Next ChapterXVII. Further Reading | — | ||||||

| 5/12/26 |  MARA Holdings: From Penny Stock to Bitcoin's Bellwether - $MARA | From a failing penny-stock patent troll to one of the world's largest Bitcoin mining behemoths, the story of MARA Holdings is a masterclass in audacious corporate reinvention. In 2017, staring down the barrel of irrelevance, the company executed a radical pivot into the volatile world of cryptocurrency, sparking a wild journey marked by 96% stock crashes, near-death experiences, and multi-billion-dollar triumphs. Navigating international mining bans, ESG controversies, and the collapse of key partners, MARA transformed from a vulnerable hardware renter into a vertically integrated energy and digital infrastructure titan. But as it now expands into AI and high-performance computing, a central tension remains: is this a durable, lasting enterprise, or merely a speculative bet dressed in industrial clothing? Dive into this fascinating saga to uncover how a company repeatedly defied the odds and forced the market to rethink the intersection of energy infrastructure and digital assets.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/MARAIntroduction and Episode RoadmapThe Pre-History: Marathon Patent Group (2010-2017)The Great Pivot: Discovering Bitcoin Mining (2017-2018)Building the Foundation: Early Mining Operations (2018-2020)The Explosive Growth Phase (2020-2021)Inflection Point: The China Mining Ban (Mid-2021)Inflection Point: The Energy and ESG Crisis (2021-2022)Inflection Point: Compute North Bankruptcy and Vertical Integration (2022-2023)The Modern Era: Scale, Strategy, and the 2024 HalvingTechnology and Operations Deep DiveBusiness Model and Unit EconomicsStrategy and Competitive PositioningThe Regulatory and Political EnvironmentPorter's Five Forces and Hamilton's Seven PowersBull vs. Bear CaseKey Metrics: What to WatchThe Big Questions and Future ScenariosLessons for Founders and InvestorsThe VerdictFurther Reading and Resources | — | ||||||

| 5/11/26 |  Travere Therapeutics: From Orphan Drug Pioneer to Rare Disease Powerhouse - $TVTX | Born from the wreckage of one of the pharmaceutical industry’s most notorious boardroom scandals, Travere Therapeutics has engineered an unprecedented corporate resurrection to become a multi-billion-dollar rare disease powerhouse. Shedding the toxic legacy of its infamous founder, Martin Shkreli, the company took an audacious gamble on a discarded hypertension molecule, transforming it into FILSPARI—a lifesaving, first-in-class treatment for devastating and previously untreatable kidney diseases. Through a high-stakes blend of regulatory ingenuity, unyielding patient advocacy, and brilliant scientific pivoting, Travere not only staved off financial collapse but successfully rewrote the playbook for orphan drug development. This captivating saga of near-death business experiences, fierce resilience, and breakthrough medical innovation offers a thrilling look into how a scrappy biotech underdog defied the odds to deliver hope to desperate patients and conquer the unforgiving market.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/TVTXThe Biotech Context and the Orphan Drug RevolutionOrigins: Retrophin and Martin Shkreli's Shadow (2011-2015)The Phoenix Moment: New Leadership and Strategic Reset (2015-2016)The Clinical Gamble: Betting Everything on Sparsentan (2016-2020)The Regulatory Marathon: FDA Approval Journey (2020-2023)Building the Commercial Engine (2023-Present)The Inflection Points That Changed EverythingThe Science and Patient Impact StoryBusiness Model and Unit EconomicsStrategic Analysis: Porter's Five ForcesStrategic Analysis: Hamilton's Seven PowersBull vs. Bear CaseLessons for Founders, Investors, and Biotech BuildersThe Future: Where Does Travere Go From Here?Epilogue and ReflectionsFurther Reading and Resources | — | ||||||

| 5/10/26 |  Sealed Air: The Unexpected Journey from Bubble Wrap to Packaging Platform - $SEE | From a failed garage experiment to create textured wallpaper to a $10 billion private equity buyout, the story of Sealed Air Corporation—the inventors of the iconic Bubble Wrap—is a masterclass in the chaotic realities of corporate evolution. This fascinating deep-dive explores how two engineers accidentally revolutionized the global shipping and food packaging industries, only to navigate decades of high-stakes financial engineering, disastrous acquisitions, and intense activist pressure. Discover how a business built on popping plastic bubbles transformed itself into a sophisticated "razor-and-blade" automated systems powerhouse, offering crucial lessons on the relentless tension between innovation, commoditization, and survival in the cutthroat industrial world.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/SEEI. Introduction & Episode RoadmapII. The Invention Era: Bubble Wrap & Early Innovation (1957-1970s)III. Building the Moat: Scale, Patents, and Category Leadership (1970s-1990s)IV. The Leveraged Recapitalization and the Cryovac Gambit (1989-2008)V. The Diversey Acquisition: Doubling Down or Doubling Trouble? (2011)VI. The Transformation Decade: Activism, Divestitures & Reinvention (2013-2020)VII. The Pandemic Pivot & Recent Evolution (2020-2024)VIII. The CEO Carousel and the Road to Going Private (2023-2026)IX. Business Model Deep Dive: The Razor-Razorblade EvolutionX. Competitive Analysis: Porter's Five Forces & Hamilton's Seven PowersXI. Playbook: Business & Investing LessonsXII. Bull vs. Bear Case & Investment ConsiderationsXIII. Epilogue: What Comes Next for Sealed AirXIV. References & Further Reading | — | ||||||

| 5/9/26 |  MEDNAX.: The Rise, Fall, and Transformation of America's Physician Outsourcing Empire - $MD | From its visionary origins in a 1970s Florida neonatal intensive care unit to its peak as a $7 billion physician-staffing colossus, the story of MEDNAX Inc. (now Pediatrix Medical Group) is a riveting masterclass in the perils of corporate healthcare consolidation. What began as a genuine solution to a critical shortage of specialized doctors transformed into a sprawling empire built on aggressive acquisitions and the highly controversial practice of "surprise billing." When this lucrative but politically toxic strategy collided with a bipartisan legislative crackdown and a once-in-a-century pandemic, the company faced a catastrophic reckoning that nearly erased it from the map. Dive into this dramatic tale of hubris, regulatory arbitrage, and a desperate fight for survival to discover how a business that stood between hospitals and their most vital physicians became one of the most instructive cautionary tales in modern American medicine.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/MDI. Introduction & Episode RoadmapII. The Founding Story & Birth of Pediatrix (1979–1995)III. Going Public & The Roll-Up Machine (1995–2008)IV. The Golden Age: Peak Roll-Up & Diversification (2008–2015)V. The Unraveling: Surprise Billing, Reimbursement Cuts & Management Turmoil (2016–2020)VI. COVID-19 & The Perfect Storm (2020–2021)VII. Transformation & The Turnaround Attempt (2021–Present)VIII. The Competitive Landscape & Industry EvolutionIX. Playbook: Business & Investing LessonsX. Porter's 5 Forces & Hamilton's 7 Powers AnalysisXI. Bull vs. Bear Case & Future OutlookXII. Epilogue & ReflectionsXIII. Further Reading & Resources | — | ||||||

| 5/8/26 |  Lyft: The Underdog Story of Ride-Sharing's Pink Mustache - $LYFT | Discover the captivating underdog story of Lyft, the ride-sharing pioneer that strapped pink fuzzy mustaches to its cars and dared to challenge the ruthless juggernaut of Uber. Born from a revelation in a Zimbabwean minibus, Lyft championed a community-first, friendly alternative in a transportation revolution fueled by smartphones and the gig economy. Yet, despite winning the public's affection and navigating fierce subsidy wars, high-stakes IPOs, and a devastating global pandemic, Lyft's journey exposes a harsh business reality: in a cutthroat, capital-intensive market with zero switching costs, being beloved isn't always enough to secure the crown. Dive into this fascinating case study to uncover the intricate dynamics of platform economics, the limits of corporate culture as a competitive moat, and the relentless battle for survival in one of Silicon Valley's most contested arenas.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/LYFTI. Introduction & Episode RoadmapII. The Founding Context: Why 2007–2012 Was Ripe for Ride-SharingIII. Zimride: The Unexpected Origin Story (2007–2012)IV. The Pivot: From Zimride to Lyft (2012)V. The Friendship Strategy & Culture Wars (2012–2014)VI. The Battle for Market Share: Peak Competition (2014–2017)VII. The Road to IPO: Growing Up in Public (2018–2019)VIII. The Pandemic: Existential Crisis & Resilience (2020–2021)IX. The Profitability Push & Leadership Shakeup (2022–2024)X. The Autonomous Vehicle Detour & Strategic BetsXI. Business Model Deep Dive & Unit EconomicsXII. Porter's Five Forces AnalysisXIII. Hamilton's Seven Powers AnalysisXIV. The Bull vs. Bear CaseXV. Key Lessons & Playbook ThemesXVI. The Future: What Happens NextXVII. Epilogue: Recent Developments (Late 2024–Early 2026)XVIII. Final ReflectionsXIX. Further Reading & Resources | — | ||||||

| 5/7/26 |  LegalZoom: The Story of DIY Legal Services - $LZ | LegalZoom successfully democratized legal services, transforming a once-exclusive, high-cost industry into an affordable, online reality for millions of small business owners. However, the company's turbulent journey from a disruptive dot-com startup to a multi-billion-dollar IPO—and its subsequent dramatic stock collapse—reveals a fascinating paradox: breaking open a market does not guarantee you can profitably own it. As LegalZoom navigates relentless competition, shifting regulatory hurdles, and the looming existential threat of artificial intelligence, its story serves as a gripping case study on the limits of brand power and the struggle to build a durable economic moat. Dive into this comprehensive breakdown to explore how a simple $79 LLC formation challenged a centuries-old monopoly, and discover whether LegalZoom's latest strategic pivot will secure its future or seal its fate as a cautionary tale of the digital age.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/LZI. Introduction & Episode RoadmapII. The Legal Industry Before LegalZoomIII. Founding Story: Four Guys and a Revolutionary IdeaIV. The Growth Years: Scaling Through MarketingV. The Attorney Network and the Hybrid ModelVI. The First IPO Attempt and the Private Equity EraVII. Going Public: The IPO and the EuphoriaVIII. Crisis and Transformation: The Pressure CookerIX. The Inflection Point: Survive or Thrive?X. Business Model Deep Dive and Unit EconomicsXI. Porter's Five ForcesXII. Hamilton's Seven PowersXIII. Bear Case vs. Bull CaseXIV. Lessons for Founders and InvestorsXV. Epilogue: The Future of Legal ServicesXVI. Sources and Further Reading | — | ||||||

Want analysis for the episodes below?Free for Pro Submit a request, we'll have your selected episodes analyzed within an hour. Free, at no cost to you, for Pro users. | |||||||||

| 5/6/26 |  Nu Skin Enterprises: The Multi-Level Marketing Empire That Went Digital - $NUS | From its scrappy 1984 beginnings in a Provo apartment to its meteoric rise as a multi-billion-dollar skincare empire, Nu Skin Enterprises has spent four decades straddling the volatile line between legitimate consumer success and the regulatory crosshairs of the multi-level marketing (MLM) world. This deep dive traces the company’s dramatic journey: a "golden era" fueled by a massive bet on the Chinese middle class that ended in a staggering $3 billion market-cap wipeout, followed by a high-stakes pivot from hotel ballroom meetings to a digital-first "social commerce" platform. As the company grapples with shrinking affiliate counts and a crashing stock price, it is now doubling down on a futuristic identity as an AI-powered beauty tech firm, utilizing handheld scanners and biometric data to stay relevant in the age of the creator economy. Nu Skin’s story is a masterclass in geographic concentration risk and corporate resilience, posing a provocative question for any investor or entrepreneur: can a legacy distribution model actually survive the disruption of TikTok and direct-to-consumer giants, or is this "empire" in a state of terminal decline?---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/NUSI. Introduction & Episode RoadmapII. The MLM Industry Context & Nu Skin's Origins (1984–1990s)III. International Expansion & The Asian Opportunity (1990s–2000s)IV. The China Dream & Nightmare (1998–2006)V. The Pharmanex Acquisition & Wellness Pivot (1998)VI. The Golden Era & Mainland China Explosion (2006–2014)VII. Crisis & The Chinese Crackdown (2014–2017)VIII. The Comeback Plan: Digital Transformation & Social Commerce (2017–2020)IX. The Pandemic Pivot & Rhyz Launch (2020–2022)X. Modern Era: The AI Beauty Device Company (2022–Present)XI. Porter's Five Forces AnalysisXII. Hamilton's Seven Powers FrameworkXIII. Business Model Deep Dive & The MLM QuestionXIV. Playbook: Business & Investing LessonsXV. Bear vs. Bull Case & Investment ConsiderationsXVI. Epilogue: What Does the Future Hold?XVII. Further Reading & Resources | — | ||||||

| 5/5/26 |  Semtech Corporation: The Quiet Giant Behind IoT's Infrastructure - $SMTC | Discover the fascinating evolution of Semtech Corporation, a quiet, sixty-five-year-old analog semiconductor company that unexpectedly became the invisible backbone of the modern connected world. From its humble origins manufacturing military components to a near-fatal financial crisis, Semtech reinvented itself through a brilliant $5 million acquisition that birthed LoRa—the low-power, long-range wireless standard now connecting billions of Internet of Things (IoT) devices. But the journey wasn't without peril; a disastrous $1.2 billion mega-deal nearly sank the company just as the AI infrastructure boom arrived, unexpectedly handing them a lucrative new lifeline in power-efficient data center tech. Dive into this gripping tale of strategic gambles, standards wars against telecom giants, and the rare corporate resilience required to survive and thrive in the brutal, ever-shifting semiconductor industry.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/SMTCI. Introduction and Episode RoadmapII. The Semiconductor Landscape and Semtech's OriginsIII. The Lost Decade: Acquisitions Without Direction (2000-2011)IV. The LoRa Acquisition: Semtech's Defining Bet (2012)V. Building the LoRa Ecosystem: Network Effects and Platform Strategy (2014-2018)VI. Portfolio Diversification: Beyond LoRa (2015-2020)VII. The Sierra Wireless Mega-Deal and Integration (2023)VIII. Navigating the 2022-2024 Semiconductor DownturnIX. The Competitive Landscape and Market Position (2024-Present)X. Business Model Deep Dive and Unit EconomicsXI. Porter's Five Forces AnalysisXII. Hamilton's Seven Powers AnalysisXIII. The Bull vs. Bear DebateXIV. Key Performance Indicators: What to WatchXV. Lessons for Founders, Operators, and InvestorsXVI. Epilogue: The Road AheadXVII. Further Reading and Resources | — | ||||||

| 5/4/26 |  Hanover Insurance Group: From New England Fire Insurer to Specialty P&C Powerhouse - $THG | From its origins insuring tinderbox buildings in 1852 Manhattan to surviving the 1906 San Francisco earthquake and a near-fatal corporate collapse in the early 2000s, The Hanover Insurance Group’s story is a gripping masterclass in resilience and reinvention. Once a stagnant personal lines carrier dangerously close to being sold for parts, Hanover executed one of the most remarkable turnarounds in modern finance by ruthlessly pivoting toward specialty commercial insurance and uncompromising underwriting discipline. Today, it stands as a highly profitable, $6 billion industry powerhouse that defies our tech-obsessed era, proving that deep risk expertise, enduring independent agent relationships, and a cultural devotion to profitability over blind growth are the ultimate engines of compounding value. Dive into this fascinating journey to discover why the most seemingly "boring" businesses—when armed with unyielding discipline and an ironclad commitment to keeping their promises—often engineer the most extraordinary and enduring success stories in capitalism.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/THGIntroduction and Episode RoadmapThe Founding Era and Early Context (1850s–1900)Survival Through Crisis: From San Francisco 1906 to the Great DepressionPost-War Expansion and the State Mutual Era (1945–1990s)The Spinoff and Independence (1995): Rebirth as a Public CompanyThe Catastrophe Years and Near-Death Experience (2000–2005)The Turnaround: Enter Fred Eppinger (2003–2016)Building the Specialty Machine (2008–2018)The Modern Era: Digital Transformation and Market Leadership (2017–Present)The Business Model Deep DiveCompetitive Landscape and Industry DynamicsPorter's Five Forces AnalysisHamilton's Seven Powers AnalysisBull vs. Bear CaseLessons and Playbook for Founders and InvestorsEpilogue: The Road AheadFurther Reading and Resources | — | ||||||

| 5/3/26 |  Palomar Holdings: The Story of a Data-Driven Insurgent in Specialty Insurance - $PLMR | How did a small team of industry veterans build a $3 billion specialty insurer from scratch in under a decade without falling into the notorious "InsurTech" trap? The answer lies in the fascinating trajectory of Palomar Holdings. By targeting the massive, underserved market of California earthquake insurance, Palomar deployed advanced data analytics and granular underwriting discipline not as flashy gimmicks, but as genuine enablers of profitable risk management. While high-profile startups burned billions trying to "disrupt" the industry, Palomar quietly expanded its catastrophe-focused portfolio to achieve explosive, highly profitable growth amid historic disasters and market turbulence. Dive into the full article to discover how this data-driven insurgent combines cutting-edge technology with old-school insurance fundamentals, offering a compelling masterclass in counter-cyclical strategy, rigorous capital allocation, and the art of building a durable competitive moat in one of the world's most volatile industries.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/PLMRI. Introduction and Episode RoadmapII. Founding Context: The Specialty Insurance Opportunity (2014)III. Building the Foundation: Strategy and Early Products (2014–2017)IV. The IPO Decision: Going Public at Scale (2019)V. Product Expansion and Geographic Diversification (2017–2020)VI. Key Inflection Point: COVID-19 and Market Dislocation (2020)VII. Key Inflection Point: The Hard Market and Pricing Power (2020–2022)VIII. The Maui Wildfire Test: When Catastrophe Strikes (August 2023)IX. Recent Developments and Current State (2023–2025)X. The Technology and Data MoatXI. Business Model Deep DiveXII. Competitive Landscape and Strategic AnalysisXIII. Analytical Framework: Porter's Five Forces and Hamilton's Seven PowersXIV. Bull versus Bear CaseXV. Lessons for Founders and InvestorsXVI. What the Future HoldsXVII. Epilogue and Final ReflectionsXVIII. Further Reading and Resources | — | ||||||

| 5/2/26 |  Spire: The Story of America's Gas Utility Consolidator - $SR | From its origins lighting the streets of pre-Civil War St. Louis to its modern status as a multi-state energy titan, Spire Inc. (SR) has spent 169 years mastering the art of quiet compounding. This is far from the story of a "boring" utility; it is a high-stakes chronicle of a company that transformed from a regional provider into an aggressive M&A platform, navigating a dramatic federal court battle over a controversial pipeline and making a multi-billion-dollar bet on the rapid growth of Nashville. As the world pushes toward electrification, Spire faces an existential crossroads: can a century-old infrastructure giant successfully pivot to a decarbonized future, or will its massive network of pipes become a stranded relic of a bygone era? Step inside the hidden world of regulated economics to discover how Spire plays a sophisticated regulatory chess game, proving that even the most stable dividend payers are often hiding the most fascinating strategic battles.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/SRI. Introduction and Episode RoadmapII. The Early Days: Gaslight and Industrial America (1857-1940s)III. The Regulated Utility Business Model: A Deep DiveIV. The Laclede Gas Era: St. Louis Consolidation and Stability (1950s-2000)V. The Roll-Up Strategy Begins: Alabama Acquisitions (2000s-2014)VI. The Rebrand and Laclede/Alagasco Integration: Becoming Spire (2014-2016)VII. Spire Storage and the Pipeline Controversy (2016-2021)VIII. Geographic Expansion and Recent M&A Activity (2017-Present)IX. The Energy Transition Dilemma: Gas Utilities in a Decarbonizing World (2018-Present)X. Modern Business Deep Dive: Operations, Culture, and Strategy (2020-Present)XI. The Regulatory Chess Game: Rate Cases and ReturnsXII. Playbook: Business and Investing LessonsXIII. Analytical Frameworks: Porter's Five Forces and Hamilton's Seven PowersXIV. Bull vs. Bear Case and Investment ConsiderationsXV. Epilogue: The Utility in TransitionXVI. Further Reading and Resources | — | ||||||

| 5/1/26 |  Taylor Morrison Home Corporation: Building the American Dream - $TMHC | Born from the wreckage of the 2008 housing crisis through one of the boldest contrarian bets in real estate history, Taylor Morrison has quietly transformed into an $8 billion national homebuilding empire. Under the trailblazing leadership of Sheryl Palmer, the company defied industry norms by targeting move-up and luxury buyers, executing perfectly timed acquisitions, and pivoting to a resilient, capital-light land strategy. This isn't just a corporate history; it is a masterclass in turning cyclical devastation into a durable competitive moat. Dive into the fascinating story of how Taylor Morrison built a powerhouse out of the market's ashes, and discover the strategic playbook that allows them to continuously thrive through pandemics, historic interest rate shocks, and the ever-shifting landscape of the American Dream.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/TMHCI. Introduction & Episode RoadmapII. The Homebuilding Industry Context & Founding StoryIII. The Great Housing Bubble & Crash (2004-2011)IV. The Mega-Merger: Creating Taylor Morrison (2011)V. Going Public & The Housing Recovery Ride (2013-2016)VI. The William Lyon Homes Acquisition: Going Bigger (2019)VII. COVID, Boom Times, and Strategic Repositioning (2020-2022)VIII. The New Normal: Rising Rates & Adaptation (2023-Present)IX. The Taylor Morrison Operating Model & Competitive MoatsX. Porter's Five Forces & Hamilton's Seven Powers AnalysisXI. Bull vs. Bear Case & What to WatchXII. Epilogue & Future OutlookXIII. Resources & Further Reading | — | ||||||

| 4/30/26 |  Cal-Maine Foods: The Industrialization of the Egg - $CALM | Behind the anonymous cartons of white and brown eggs in nearly every American supermarket lies Cal-Maine Foods, a Mississippi-based titan that quietly produces one out of every five eggs in the United States. While the humble egg might seem like the "perfect commodity," Cal-Maine has spent nearly seventy years transforming it into a masterclass of industrial logistics, ruthless consolidation, and strategic capital allocation. By leveraging a unique "variable dividend" policy and turning industry-crushing avian flu outbreaks into massive windfalls, this family-controlled empire has consolidated 20% of a once-fragmented market. From the high-stakes regulatory battles over cage-free hens to the hidden "process power" of biosecurity, the story of Cal-Maine reveals how a business of "biological manufacturing" became one of the most resilient and fascinating corporate case studies in the modern American economy.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/CALMI. Introduction: The Commodity KingII. The "Roll-Up" Origins & Modern ContextIII. Key Inflection Point: The Great Avian Flu & The 2015 PivotIV. M&A Strategy & Capital DeploymentV. Current Management: The Sherman Miller EraVI. The "Hidden" Growth: The Specialty SegmentVII. The Playbook: Hamilton's 7 Powers & Porter's 5 ForcesVIII. Analysis: Bear vs. Bull CaseIX. Conclusion & Final Reflections | — | ||||||

| 4/29/26 |  SAP: The Empire of Enterprise Software - $SAP | From a bold IBM exodus in 1972 to becoming the backbone of global commerce, SAP’s journey is a riveting saga of engineering rigor, relentless reinvention, and strategic mastery in enterprise software. Born from five visionary engineers’ refusal to abandon a revolutionary idea, SAP evolved from scrappy beginnings to command 77% of global transaction revenue, powering everything from your morning coffee purchase to multinational supply chains. Yet beneath this colossal success lies a paradox: SAP’s software is famously complex and “boring,” lacking Silicon Valley glamour but embodying essential infrastructure few dare replace. Navigating seismic shifts—from mainframe to client-server, on-premises to cloud, and now AI-powered intelligent systems—SAP has weathered fierce competition, customer revolt, and towering technical debt while orchestrating a sprawling acquisition spree to rewrite its cloud narrative. With the 2027 deadline looming for customers to adopt its next-gen S/4HANA suite, and AI integration reshaping its future, SAP stands at a crossroads of opportunity and risk. Dive deeper to uncover how this German titan’s artful creation of near-inescapable switching costs, partnership ecosystems, and platform economics secured its empire — and what challenges lie ahead in the relentless march of technology and transformation.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/SAPI. Introduction & Episode SetupII. The IBM Exodus & Founding Story (1972)III. Building the Platform: R/1, R/2, and Early Dominance (1973–1991)IV. The R/3 Revolution & Global Domination (1992–2009)V. The Cloud Awakening & Acquisition Spree (2010–2018)VI. The Qualtrics Drama & Experience Data Play (2018–2021)VII. S/4HANA & The 2027 DeadlineVIII. RISE with SAP & Cloud Transformation (2021–Present)IX. Playbook: The Art of Enterprise Software DominanceX. Bear vs. Bull Case & Competitive AnalysisXI. Power Analysis & Future ScenariosXII. Epilogue: Lessons for BuildersXIII. Recent NewsXIV. Links & ReferencesConclusion: The Perpetual Transformation Machine | — | ||||||

| 4/28/26 |  Automatic Data Processing: The Payroll Processing Powerhouse - $ADP | From a modest storefront in 1949 to a $20.6 billion juggernaut in 2025, Automatic Data Processing (ADP) has quietly reshaped how America gets paid—processing payroll for one in seven workers and powering the backbone of HR management worldwide. This riveting journey reveals more than technological innovation; it's a masterclass in building an unshakeable business by embracing complexity, operational excellence, and strategic patience. From surviving the Wall Street Paperwork Crisis to pioneering the Professional Employer Organization model, and from deftly spinning off billion-dollar divisions to boldly transforming into a cloud-powered, AI-savvy platform, ADP’s story is one of relentless adaptation and trust built over decades. Dive into this compelling narrative to uncover how a company many overlook teaches profound lessons on resilience, scale, and the quiet power of doing the essential well—year after year.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/ADPIntroduction and Episode SetupOrigins: The Taub Brothers and Manual Payroll Processing (1949–1961)Going Public and Early Computer Adoption (1957–1970)Wall Street Crisis and the Brokerage Business (1968–1985)The PEO Revolution and Expansion (1990s–2000s)The Spinoff Era: Broadridge and CDK Global (2007–2014)Modern ADP: Technology and Scale (2008–Present)Business Model Deep DiveFinancial Performance and Market PositionPlaybook: Strategic and Investing LessonsAnalysis and Investment CaseFuture Outlook and Key QuestionsRecent News | — | ||||||

| 4/27/26 |  LiveRamp: The Identity Fabric of Digital Advertising - $RAMP | LiveRamp is the invisible engine quietly orchestrating the $700 billion digital advertising industry, acting as a "universal translator" that securely bridges the gap between offline consumer data and online digital identities. Born from a legacy data broker and forged in the fires of strict global privacy regulations like GDPR, this unsung tech giant has successfully positioned itself as the neutral "Switzerland of ad tech." By offering a privacy-first, cookie-less infrastructure that top brands, publishers, and booming retail media networks desperately rely on, LiveRamp has built a formidable empire around authenticated identity and secure data clean rooms. But as massive cloud platforms and open-source alternatives begin to encroach on its territory, can the company maintain its competitive moat? Dive into the fascinating corporate evolution, high-stakes platform wars, and precarious future of the indispensable middleman that secretly powers the internet's attention economy.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/RAMPI. Introduction & Episode RoadmapII. Prehistory: Acxiom's Data Empire & the Rapleaf AcquisitionIII. The Data Onboarding Gold Rush (2014-2017)IV. The Spin-Off: Creating a Pure-Play Identity Company (2018)V. GDPR, CCPA & The Privacy Reckoning (2018-2020)VI. The Chrome Cookie Deprecation Saga (2020-Present)VII. The Architecture Play: Safe Haven & Clean Rooms (2019-Present)VIII. Retail Media & The Bezos Problem (2020-Present)IX. The Business Model Evolution & Unit EconomicsX. The Competitive Landscape & Market StructureXI. Inflection Point: Connected TV & Streaming Wars (2021-Present)XII. International Expansion & Regulatory DivergenceXIII. Porter's Five Forces & Market DynamicsXIV. Hamilton's Seven Powers & Strategic Moat AssessmentXV. Bull vs. Bear CaseXVI. The Strategy Tax & Organizational ChallengesXVII. What's Next: AI, Privacy, & the Future of IdentityXVIII. Epilogue & ReflectionXIX. Further Reading & Resources | — | ||||||

| 4/26/26 |  Virtus Investment Partners: The Story of a Multi-Boutique Asset Manager - $VRTS | Born from the ashes of a struggling insurance parent at the absolute peak of the 2008 financial crisis, Virtus Investment Partners is one of modern finance’s most captivating underdog stories. While the relentless rise of cheap, passive index funds has destroyed countless active managers, Virtus defied the odds to grow its assets to over $150 billion by mastering the "multi-boutique" model—acquiring specialized, highly autonomous investment teams and letting them flourish while handling their operational and distribution hurdles behind the scenes. This deep dive explores the high-stakes art of the corporate roll-up, the firm's strategic pivot into lucrative private credit, and the existential battle between human financial expertise and algorithmic indexing. Whether you are an investor, a founder, or simply fascinated by brilliant corporate survival strategies, this piece pulls back the curtain on the hidden mechanics of the asset management industry and invites you to discover what it truly takes to thrive when the deck is heavily stacked against you.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/VRTSI. Introduction & Episode RoadmapII. The Phoenix Companies Origins & Early History (1851-2000s)III. The Spin-Off and the Worst Timing in Financial History (2005-2008)IV. Going Public & Finding an Identity (2009-2013)V. The Multi-Boutique Transformation: Strategic Inflection (2014-2017)VI. Scaling Up Through Strategic Partnerships (2017-2019)VII. Weathering Volatility & Continuing the Roll-Up (2018-2020)VIII. Market Boom & The Alternatives Push (2020-2022)IX. The New Era: Navigating Headwinds and Pivoting to Private Credit (2022-Present)X. The Multi-Boutique Business Model Deep DiveXI. Industry Context & Competitive LandscapeXII. Porter's 5 Forces & Hamilton's 7 Powers AnalysisXIII. Bull vs. Bear CaseXIV. Playbook: Lessons for Founders & InvestorsXV. Epilogue & Future OutlookXVI. Further Reading & Resources | — | ||||||

| 4/25/26 |  Worthington Enterprises: Building Value Through Steel, Strategy, and Culture - $WOR | From a humble $600 loan to buy a single load of steel in 1955, Worthington Enterprises built a multi-billion-dollar industrial empire fueled by a radical, decades-long commitment to the "Golden Rule" and fierce employee loyalty. Yet, after nearly seventy years of weathering economic storms through disciplined diversification, the company recently executed one of the most remarkable strategic pivots in modern manufacturing: it spun off its founding steel business entirely. This bold transformation shifted Worthington from a cyclical commodity processor into a high-margin powerhouse of recognizable consumer brands, essential building products, and cutting-edge hydrogen infrastructure. Dive into the fascinating story of how a family-run business survived crushing recessions, defied Wall Street's short-term pressures, and ultimately found the courage to shed its very identity to forge a more profitable, future-proof legacy.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/WORI. Introduction and Episode RoadmapII. Founding Story and The John McConnell Vision (1955-1970s)III. Building the Steel Processing Empire (1970s-1990s)IV. The Diversification Era and Building the Portfolio (1990s-2000s)V. The Great Recession and Resilience Test (2008-2010)VI. The Transformation Inflection Point: 2010s Strategic ShiftsVII. The WAVE Joint Venture and Cylinders Dominance (2017-2020)VIII. The Radical Pivot: The Steel Spinoff Decision (2022-2024)IX. Worthington Enterprises Today: The New Company (2024-Present)X. The Business Model and Competitive DynamicsXI. Porter's Five Forces AnalysisXII. Hamilton's Seven Powers Framework AnalysisXIII. The Playbook: Business and Strategic LessonsXIV. Bull Case, Bear Case, and Investment ThesisXV. Recent Developments and Looking ForwardXVI. Epilogue and Final ReflectionsXVII. Further Reading and Resources | — | ||||||

| 4/24/26 |  Yelp: The Story of the Original Review Platform - $YELP | Long before AI chatbots and visual social media algorithms dictated our dining and spending habits, Yelp revolutionized local commerce by turning crowdsourced opinions into a billion-dollar empire. Born from the legendary "PayPal Mafia," the platform has spent two decades navigating a gauntlet of existential threats, surviving brutal distribution battles with Google, public relations nightmares over extortion allegations, and the sudden devastation of a global pandemic. Yet, while Yelp remains highly profitable today through a savvy pivot to the home services market, the original pioneer of online trust now stands at a fascinating crossroads. Dive into the complex story of Yelp’s rise to cultural ubiquity, explore the strategic triumphs and missteps that defined its fierce independence, and discover why the ultimate test of its 330-million-review moat will be surviving the dawn of the artificial intelligence era.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/YELPI. Introduction & Episode RoadmapII. The PayPal Mafia & Silicon Valley Context (2004)III. The Pivot & Finding Product-Market Fit (2004–2006)IV. Monetization & The Extortion Controversy (2007–2010)V. The Google Existential Threat (2010–2014)VI. The Mobile Revolution & International Expansion (2011–2015)VII. The Grubhub Era & Strategic Missteps (2015–2017)VIII. The Amazon & Platform Threats (2015–2020)IX. COVID-19: Crisis & Adaptation (2020–2021)X. The Modern Era: AI, Competition & Reinvention (2021–Present)XI. Business Model Deep Dive & Unit EconomicsXII. Playbook: Business & Investing LessonsXIII. Porter's Five Forces AnalysisXIV. Hamilton's Seven Powers AnalysisXV. Bear vs. Bull CaseXVI. Epilogue & The FutureXVII. Further Reading & Resources | — | ||||||

| 4/23/26 |  Knight-Swift: The Consolidation of the American Highway - $KNX | Knight-Swift Transportation Holdings is far more than a sprawling fleet of trucks; it is a masterclass in how surgical operational discipline can transform a cutthroat commodity business into a high-moat logistics powerhouse. From its roots as a lean Phoenix startup founded on an obsession with "operating ratios" to its transformative reverse takeover of Swift and recent pivot into the high-margin world of Less-Than-Truckload (LTL) shipping, the company has methodically engineered a proprietary management system that outpaces the brutal cycles of the American freight market. Under a new generation of leadership, Knight-Swift is now evolving into a diversified, tech-driven platform that turns competitors into customers and distressed assets into profit engines. Dig into this deep dive to discover how the "Knight Playbook" is quietly consolidating the American highway and why this logistics giant might be the most misunderstood industrial story hiding in plain sight.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/KNXI. Introduction and The "Freight King" ThesisII. Roots: The Knight Brothers and the Birth of DisciplineIII. The 2017 Merger: A "Reverse Takeover" in DisguiseIV. M&A Strategy: Buying the MoatV. Current Management: The Adam Miller EraVI. Hidden Gems: Beyond the Big RigVII. Framework Analysis: 7 Powers and 5 ForcesVIII. Playbook: Business and Investing LessonsIX. Analysis: Bear vs. Bull CaseX. Epilogue and Final ReflectionsXI. Further Reading | — | ||||||

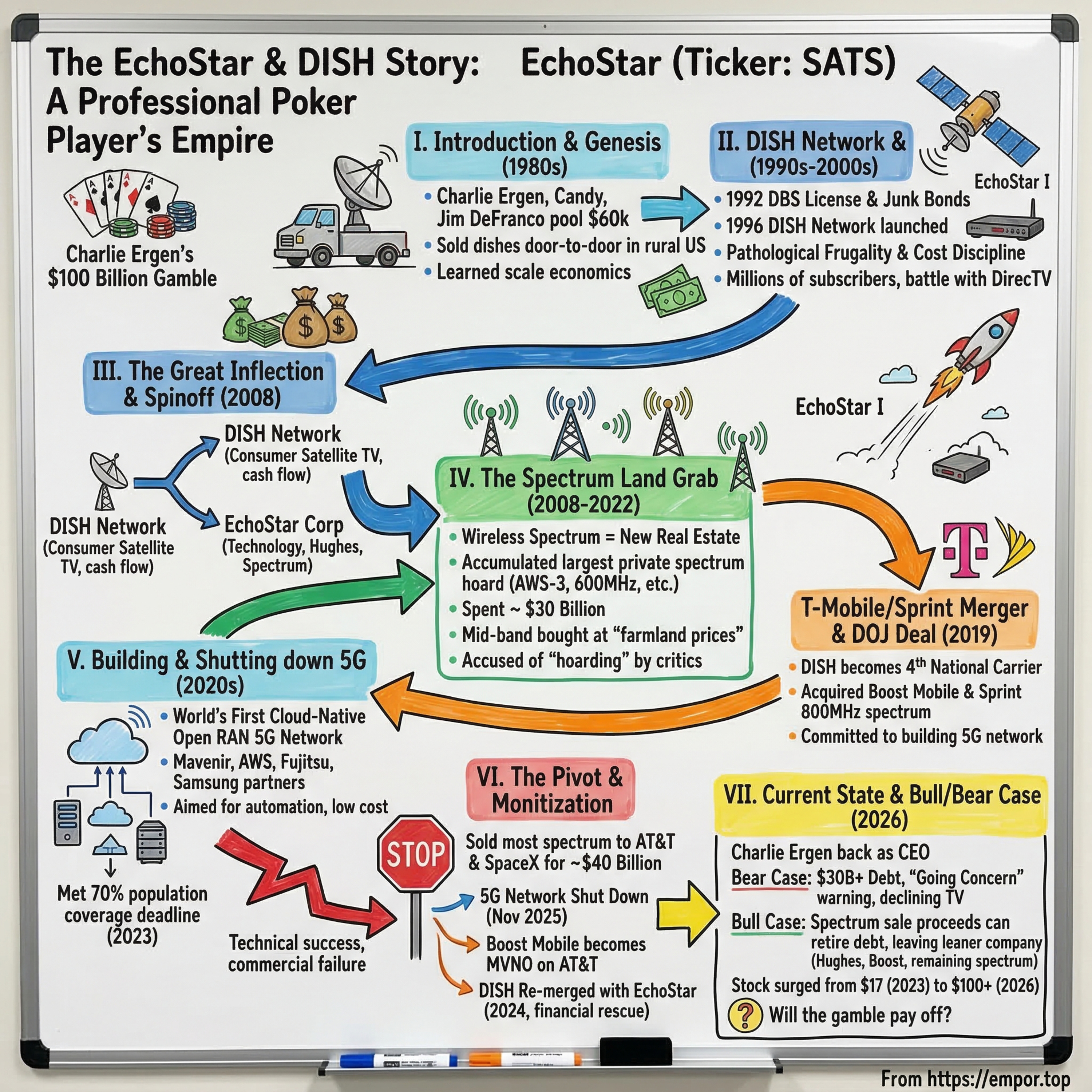

| 4/22/26 |  The EchoStar and DISH Story: The Professional Poker Player's Empire - $SATS | From counting cards in Lake Tahoe to orchestrating a $100 billion gamble on the future of American connectivity, Charlie Ergen’s journey with EchoStar and DISH is anything but a standard corporate biography. This deep dive explores how a door-to-door satellite dish salesman transformed into a "spectrum hoarder," quietly accumulating a massive hoard of invisible airwaves that he is now liquidating for a staggering $40 billion to industry giants like AT&T and Elon Musk’s SpaceX. As the company teeters between a "going concern" warning and a historic stock surge, the article unpacks a high-stakes saga of debt, vision, and the ultimate poker play. Will Ergen be vindicated as a generational genius or remembered for a spectacular telecom collapse? Step inside the boardroom to see how the final hand of this forty-year drama is being dealt.---Subscribe to our newsletter on LinkedIn https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7408775804387491842Follow us on X @emportop---Transcript - https://empor.top/us/SATSI. Introduction: The $100 Billion GambleII. The Genesis: From the Back of a Truck to the SkyIII. The Great Inflection: The 2008 Spinoff and the Spectrum Land GrabIV. The "New" EchoStar: Management and the Ergen DoctrineV. M&A Deep Dive: The Boost Mobile Acquisition and the DISH Re-MergerVI. The Hidden Businesses: Beyond the Satellite DishVII. The Playbook: Strategic AnalysisVIII. Bear vs. Bull CaseIX. Conclusion: The Narrative ArcX. Epilogue: The Latest Hand | — | ||||||

Showing 25 of 220

Sponsor Intelligence

Sign in to see which brands sponsor this podcast, their ad offers, and promo codes.

Chart Positions

2 placements across 2 markets.

Chart Positions

2 placements across 2 markets.