Insights from recent episode analysis

Audience Interest

Podcast Focus

Publishing Consistency

Platform Reach

Insights are generated by CastFox AI using publicly available data, episode content, and proprietary models.

Most discussed topics

Brands & references

Total monthly reach

Estimated from 1 chart position in 1 market.

By chart position

- 🇭🇰HK · Investing#933K to 10K

- Per-Episode Audience

Est. listeners per new episode within ~30 days

900 to 3K🎙 Daily cadence·261 episodes·Last published 3d ago - Monthly Reach

Unique listeners across all episodes (30 days)

3K to 10K🇭🇰100% - Active Followers

Loyal subscribers who consistently listen

1.2K to 4K

Market Insights

Platform Distribution

Reach across major podcast platforms, updated hourly

Total Followers

—

Total Plays

—

Total Reviews

—

* Data sourced directly from platform APIs and aggregated hourly across all major podcast directories.

On the show

From 23 epsHosts

Recent guests

Recent episodes

Weekend Update - W2625

Jun 21, 2026

12m 32s

The End of the Subsidized-Token Era

Jun 20, 2026

35m 40s

The One Week We Were All in the Same Room

Jun 19, 2026

0m 58s

Weekend Update - W2624

Jun 15, 2026

11m 16s

Data Centers in Space: How SpaceX Justifies $2 Trillion

Jun 10, 2026

27m 31s

Social Links & Contact

Official channels & resources

Official Website

Login

RSS Feed

Login

| Date | Episode | Topics | Guests | Brands | Places | Keywords | Sponsor | Length | |

|---|---|---|---|---|---|---|---|---|---|

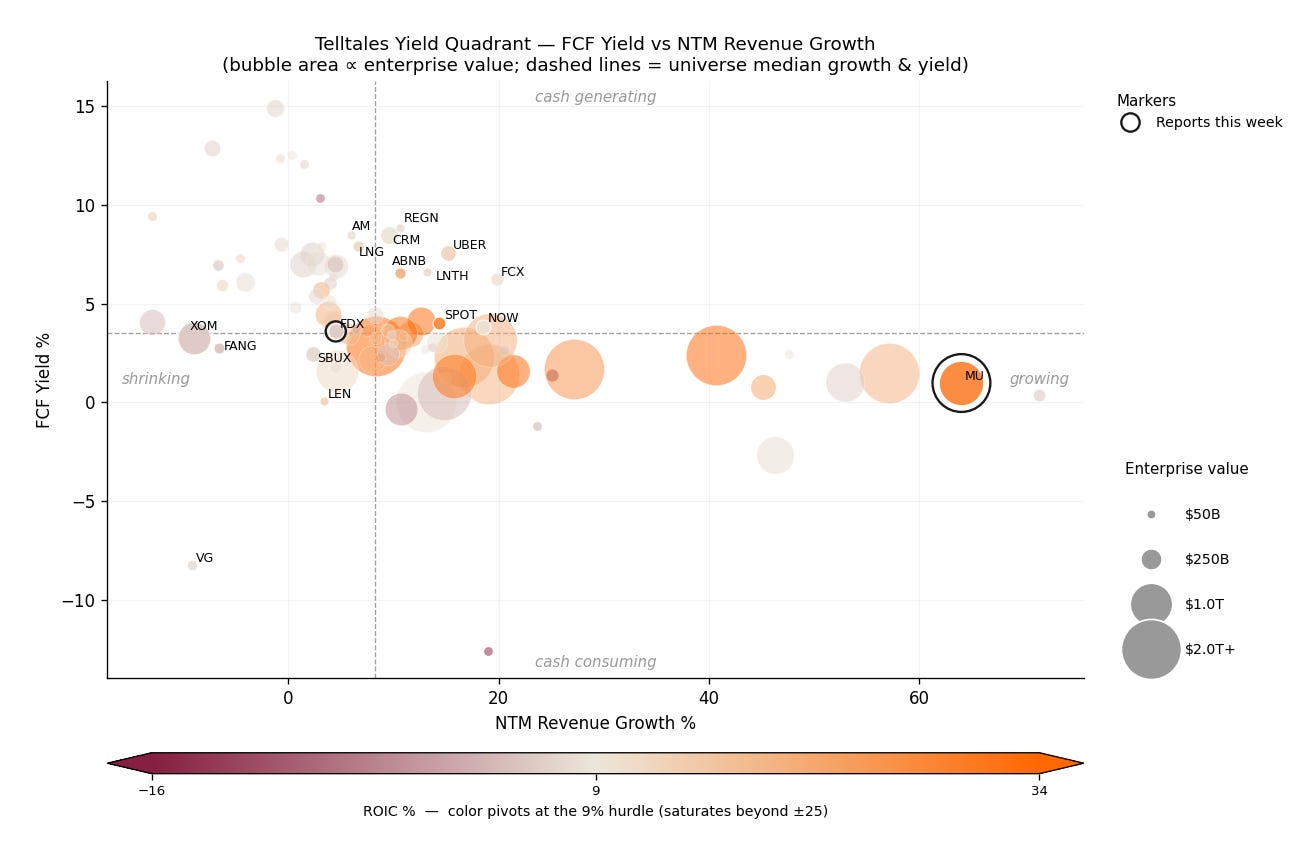

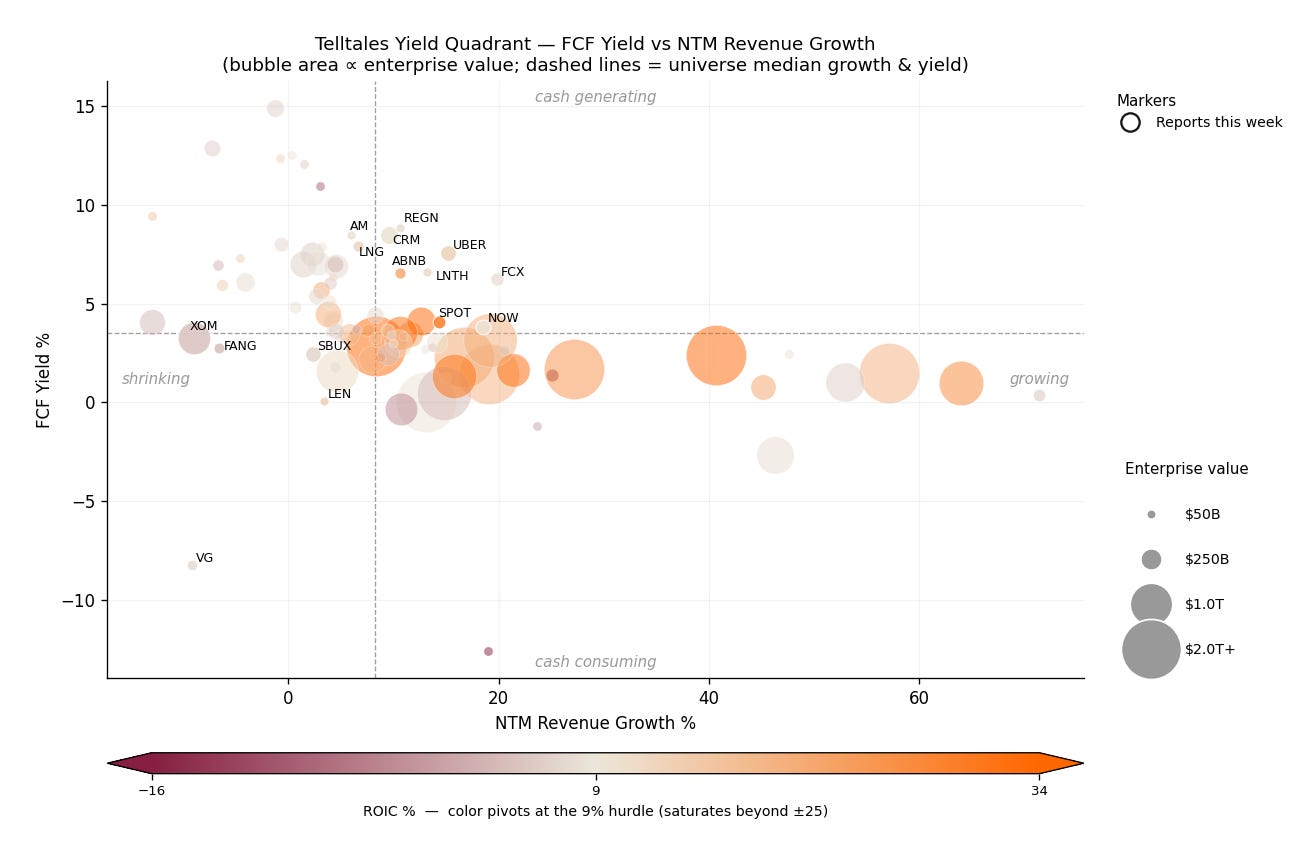

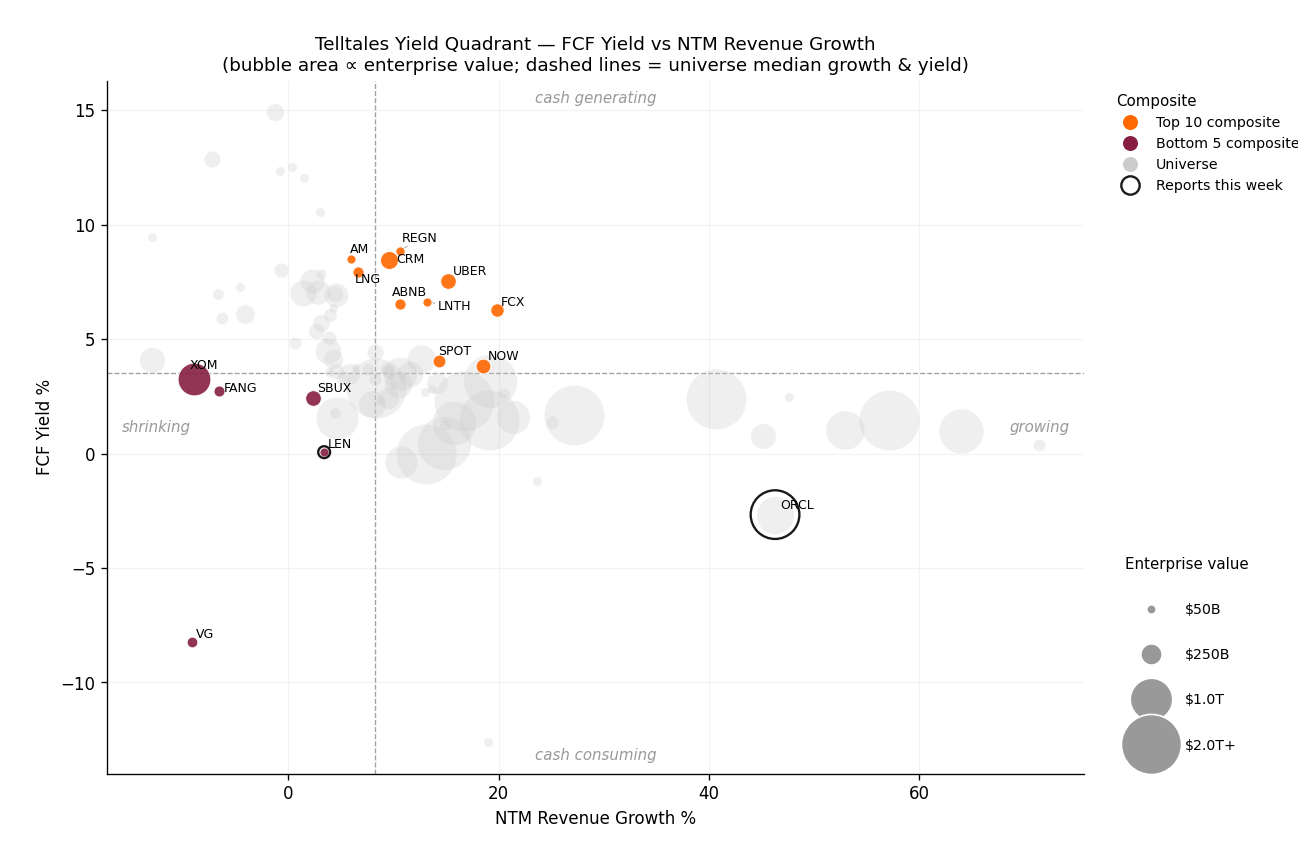

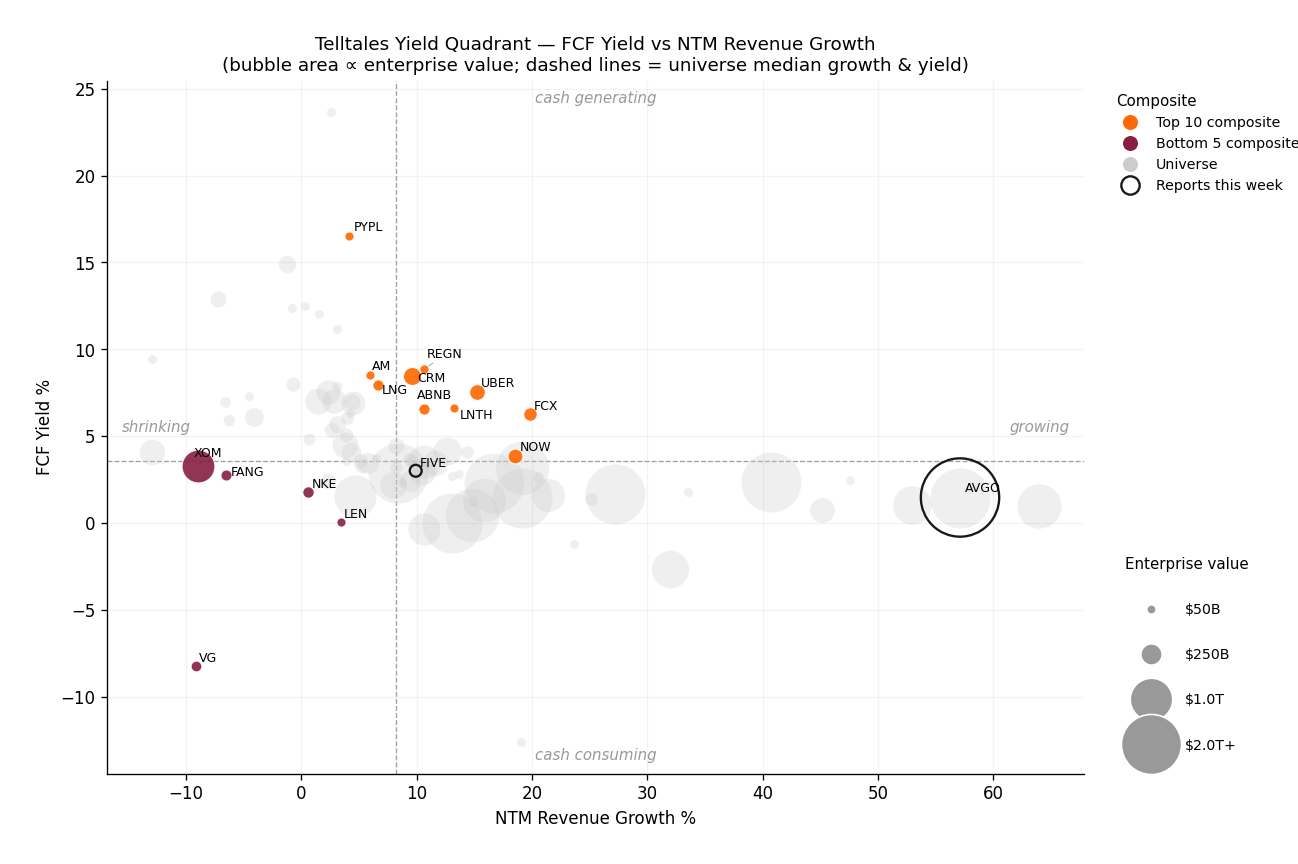

| 6/21/26 |  Weekend Update - W2625 | ▶ Explore this week’s Tape — live, sortable, drill-down →Three Bottlenecks, One Multiple, and Only One MonopolyThe AI argument flipped sides this week. For two years the only question that mattered was whether anyone would actually buy all this compute, and Wednesday’s show put that one to bed. The question left standing is whether the supply chain can physically build it — the lithography, the power, the memory. And in the rush to own the chokepoints, the market did something lazy. It paid all three the same monopoly multiple. Only one of them is a monopoly.Start with the one that is. ASML makes the machine that etches the most advanced chips on earth, and it makes it alone — no second source, no roadmap to one, no credible challenger inside a decade. The Cash Flow Memo has it trading around sixty times free cash flow, on roughly eleven billion dollars of trailing free cash flow translated from euros.¹² That is a monopoly multiple, and for once it is bolted to an actual monopoly. The thing that can dent it is not a competitor — it is a government. Commerce Secretary Howard Lutnick told ASML, per Bloomberg, that he is concerned a top-tier extreme-ultraviolet machine may have reached China in violation of export controls; the company denied it has ever shipped one there.³ Notice what the risk actually is. Not the machine. The map of who is allowed to buy it. ASML’s customer list is the only variable that has ever moved this stock, and it is the one variable ASML does not control.Now the two the market is paying as if they were ASML. GE Vernova booked more data-center power orders last quarter than it did in all of the prior year, and its turbine backlog now stretches past a hundred-ten gigawatts into 2029.⁴⁵ Free cash flow grew almost four hundred percent.⁶ Real demand, real scarcity — for now. But a gas turbine is not an EUV machine. Siemens Energy and Mitsubishi build them too, and slot scarcity is the kind of bottleneck competition fills in three or four years, not three or four decades. GE Vernova is renting its scarcity. The order book is genuine; the durability is the open question, and a thirty-times multiple is pricing the scarcity as if it were permanent.Then memory — the bottleneck with the longest rap sheet. Micron reports Wednesday with its entire 2026 high-bandwidth-memory output already sold under contract and DRAM pricing set to jump fifty percent this quarter.⁷⁸ The cashflow read is in Marcus’s column below — short version, the trailing multiple is the cheap number, not the scary one. But here is the part the show had no room for: memory is the one bottleneck on this list that has detonated itself before. Every prior cycle ended the same way. All three makers see the shortage, all three turn the capex spigot at once, supply overshoots demand, and the pricing that looked structural turns out to have been a moment. Micron is committing roughly two hundred billion dollars to new capacity, and its two competitors are spending into the same shortage.⁹ That is either supply discipline or the seed of the next glut, and you cannot tell which from inside the shortage. You never can. That is what makes memory memory.So three bottlenecks, three very different half-lives, and a tape paying all three the monopoly rate. The durable one — the cornered machine — arguably earns it. The other two are borrowing the multiple from the durable one, and the loan comes due the day a competitor adds a turbine line or a third memory maker blinks first on capex.What changes the read is Wednesday, and the tell is Micron’s gross-margin guide. Guide above where consensus already sits and the cycle is still accelerating into the glut question, not away from it.¹⁰ Merely meet it, and a sold-out company that only meets gets sold on the news. The trade across the whole supply chain breaks the moment any one of the three memory makers signals it is racing the other two to fill capacity rather than pacing itself.Wall Street’s consensus on the supply chain: own the bottleneck, any bottleneck, at any multiple. The math says own the one nobody else can build — and rent the other two only as long as the scarcity lasts.The Tape — W2625Universe of 94 cashflow-memo names, snap dates 2026-06-15 → 2026-06-19. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamMicron reports Wednesday, and the reporters table holds the whole argument in two cells that read like a contradiction: a 1.0% trailing FCF yield sitting right beside 64% forward revenue growth. Trailing, Micron screens at 102x free cash flow — and that is a cyclical at the bottom of its cash cycle, where the trailing multiple measures the past and tells you nothing about the print. The 1.0% yield is the trough. The 64% is the market pricing what sold-out capacity earns once contract prices reset higher. The cheap-looking cell is the lie; the expensive-looking one is the tell. The test Wednesday is the gross-margin guide — clear where consensus already sits with the cycle still accelerating, or a sold-out name that merely meets gets sold on the news.Telltales Yield — Bottom 10This Week’s ReportersSector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps90 of 90 ranked-eligible names ranked. 0 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-06-19.csv. NTM growth from analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoThe Week AI Became a Supply StoryThe bottleneck moved from demand to supply this week. Micron’s Wednesday print is the first real test.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the 86 companies in the Cash Flow Memo. About 13 minutes. No filler. Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode E2626.Chapter markers* Time | Segment* 0:15 | Cold open — the supply side of AI* 0:45 | Theme — the two hardest things to build (ASML, GE Vernova)* 4:45 | Deep dive — Micron, the print that sets the cycle* 8:45 | Rapid-fire — Moderna, FedEx, Nike, Cheniere, Intel* 11:45 | Close — Consensus Watch + the week aheadFull transcriptOpening disclaimerAva: The following conversation is intended for informational purposes only. You should always do your own work to determine if an investment is suitable for you.Cold openAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack. This is still a pilot, so tell us what’s working and what isn’t.Ava: And one more thing before we start — this one lands on Father’s Day. So happy Father’s Day to all the dads listening. We’re glad you’re spending part of the morning with us.Ava: Here’s the week in one sentence. The argument about whether anyone will actually buy all this AI compute? That got settled on Wednesday’s show. This week the question flipped to the other side of the ledger — can we build the supply. The machines that print the chips, the power that runs them, and the memory that feeds them. All three flashed at once. Three different stories, one spine — the build is now gated by what can physically be manufactured, not by whether the demand shows up. On this week’s Telltales, episode 2625, Hunt, Jason, and Mike spent the hour on the demand side — NVIDIA at $5 trillion, the end of the subsidized-token era, who actually pays for the compute.[^ep-e2625b] We’re taking the other half. The supply chain that has to deliver before any of that demand means a thing.Theme — The two hardest things to buildAva: Two things in this build are genuinely hard to make. One is the machine that etches the chip. The other is the electricity that runs it. Both made news this week, and both made it for the same reason — the demand has gotten ahead of the supply. Start with the machine almost nobody owns. This week the US government told the company that makes it that one of those machines may have ended up somewhere it isn’t allowed to go. US Commerce Secretary Howard Lutnick told ASML’s leadership he’s concerned one of its top-tier extreme-ultraviolet lithography machines may have reached China, in violation of export controls.[^asml-us-export-concern-20260619] ASML denied it flatly — says it has never shipped an EUV machine to China.[^asml-us-export-concern-20260619] This on the same company that just raised its full-year guide to €36–40 billion on AI demand.[^asml-q1-earnings-20260619] Marcus — what does a monopoly on the most important machine in the world actually cost?Marcus: ASML is the only company on earth that can make this machine, and the market has always paid it like one. The memo has ASML at about 62 times free cash flow,[^memo-asml-evfcf-20260619] on roughly $11 billion of trailing free cash flow, translated from euros.[^memo-asml-fcf-20260619] That’s a monopoly multiple for a monopoly. The export-control story doesn’t touch the cash — it touches who’s allowed to be a customer. And for this name, the customer list is the only variable that has ever mattered. A monopoly is worth 62 times right up until a government starts deciding who it can sell to.Ava: So the risk isn’t the machine. It’s the map of where it’s allowed to ship. And if Lutnick’s concern turns out to be real — if a top-tier machine genuinely reached China — the read-through isn’t just one company’s quarter. It’s that the export-control wall the entire AI-chip supply chain is built on has a crack in it.[^asml-us-export-concern-20260619] That’s the bigger story, and it’s why a denial isn’t the end of this one. Now the other hard thing — and it’s the boring one, right up until it’s the bottleneck. Electricity. GE Vernova booked more data-center power orders in a single quarter than it did in all of last year. $2.4 billion of electrification equipment orders for data centers in the first quarter alone.[^gev-data-center-orders-20260619] Its gas-turbine backlog now stretches past 110 gigawatts into 2029,[^gev-turbine-backlog-20260619] and Bernstein just opened coverage with an Outperform, calling it a play on the AI power boom.[^gev-bernstein-20260619] Marcus — second one. What’s the cash say?Marcus: The power names spent a decade as widow-and-orphan utilities. GE Vernova just stopped being one. The memo has it at about 33 times free cash flow,[^memo-gev-evfcf-20260619] and free cash flow grew almost 400% year over year.[^memo-gev-fcf-20260619] That’s not a utility growth rate — that’s an order book repricing to AI in real time. $2.4 billion of data-center orders in one quarter[^gev-data-center-orders-20260619] is the tell. The thing I’d watch is conversion: that backlog only matters if the turbine slots actually deliver on schedule and don’t slip. The orders are real. The execution is the open question.Deep dive — MicronAva: Now the print that sets the whole cycle. Micron — page 5 of the memo, sharing it with GE Vernova, power and memory side by side — reports Wednesday after the close,[^earn-mu] and the question isn’t whether they beat. The question is whether there’s any memory left to sell. Because Micron’s entire 2026 high-bandwidth-memory production is already sold out — every chip, under binding contract, before the year is even half over.[^mu-hbm-sold-out-20260619] And DRAM contract pricing is set to jump 50–55% this quarter alone versus the end of last year.[^mu-dram-pricing-cycle-20260619] Marcus — when the product’s sold out a year ahead, what are we actually pricing?Marcus: Here’s the trap on this one. Trailing, Micron screens at 102 times free cash flow.[^memo-mu-evfcf-20260619] Ignore that number. It’s a cyclical at the bottom of its cash-flow cycle, and a trailing multiple on a cyclical at the trough is noise — it tells you about the past, not the print. Free cash flow already grew more than 500% off the bottom,[^memo-mu-fcf-20260619] and the forward revenue line is up about 64%.[^memo-mu-ntmrev-20260619] You don’t value this on what it earned. You value it on what sold-out capacity earns at much higher pricing. And against that, 102 times trailing is the cheap number, not the scary one.Ava: So the terrifying multiple is the cheap one. Marcus’s favorite kind of sentence.Marcus: It is. And the supply side is the part the bears can’t model. Micron is committing roughly $200 billion to new capacity.[^mu-capex-expansion-20260619] You do not put $200 billion against a cycle you think is about to roll over. That’s management telling you the shortage is structural, not a head-fake. It’s the same story Nvidia’s Rubin platform is telling from the other side of the table — Micron is the qualified high-bandwidth-memory supplier into it, shipping in volume.[^mu-rubin-hbm4-20260619]Ava: And the hiring backs it up.Marcus: It does. Per the Talnexis hiring tracker, Micron is the #3 hiring floor on the entire board — 3,000 open roles, 181 of them added just this week.[^tlnx-mu-hiringfloor-20260619] You don’t staff like that into a cycle you expect to break. The one thing I’d actually watch Wednesday is the gross-margin guide — guide above where consensus already sits[^mu-margin-guidance-20260619] and the cycle’s still accelerating. Merely meet it and the stock’s already there, and a sold-out company that only meets is a sell-the-news.Ava: So what actually breaks this?Marcus: Two things, and I’d weight them. The real risk was never demand — it’s supply discipline. If all three memory makers turn the capex spigot at once, you get a glut, and the cycle ends the way every memory cycle has ended. I’d put that around 30%. The nearer risk is mix — if high-bandwidth memory crowds out standard DRAM capacity, the blended margin doesn’t reach what the Street’s penciling in. Call that another 10%. Which leaves the base case at 60% — and it’s the boring one: sold out, pricing up 50%, the capacity already committed. The cash shows up whether the multiple believes it or not.Ava: So 30% it ends in tears, 10% it just muddles through on margin, 60% it prints money — and Marcus will at least give you the whole distribution instead of selling you a price target. 81% gross margin on what used to be a commodity.[^mu-margin-guidance-20260619] Read that twice. Broadcom and Oracle spent Wednesday’s show proving the demand is real.[^ep-e2625b] Micron on Wednesday tells you whether the supply can keep up. Same trade, opposite end of the table.Rapid-fireAva: Rapid-fire. Five names, and markets open Monday.Ava: Moderna had its best week in four years, and for once it had nothing to do with COVID. An FDA advisory panel voted 9-0 to endorse its mRNA flu vaccine for adults 50 and older,[^mrna-flu-vaccine-approval-20260619] with a final FDA decision expected by August 5. The stock jumped 28%.[^mrna-stock-jump-20260619] Free cash flow is still negative here — this is an optionality name, not a cash machine — but it’s the first real commercial catalyst since the COVID franchise rolled over.Ava: Two reporters sit together on page 17 of the memo, and they’re back to back next week. FedEx is first, Tuesday after the close.[^earn-fdx] The number that matters isn’t the quarter — it’s the breakup. The Freight spinoff is on track: 80.1% of the shares distributed to FedEx holders, and Freight pays a $4.1 billion special dividend back to the parent on the way out.[^fdx-freight-spinoff-taxfree-20260619] Add $1 billion of cost cuts this year from the DRIVE program,[^fdx-drive-program-20260619] and a forward guide that just got raised.[^fdx-guidance-raise-20260619] A cleaner, lighter FedEx is the entire thesis.Ava: Nike reports the following Tuesday, June 30.[^earn-nke] This is the clearest test yet of whether Elliott Hill’s turnaround is real. The headwinds are brutal — a $1.5 billion annual tariff hit that took gross margin down 300 basis points,[^nke-tariff-cost-20260619] China down 16%,[^nke-china-decline-20260619] digital down 14%.[^nke-digital-decline-20260619] Win Now has to show up in a number Tuesday, not a slogan. First place it can.Ava: Cheniere keeps building while everyone else watches the oil price. It signed a $4.69 billion engineering contract with Bechtel for the Sabine Pass expansion,[^lng-sabine-pass-epc-20260619] with a final investment decision targeted for early 2027, and it just finished Corpus Christi Trains 5 and 6.[^lng-corpus-christi-progress-20260619] And it throws off nearly an 8% free-cash-flow yield while it does it.[^memo-lng-fcfyield-20260619] The cash machine of the energy names.Ava: And Intel had a genuinely good week on the factory floor — which is the only place that matters for this story. Its 18A-P process entered risk production: 9% more performance at the same power.[^intc-18ap-20260619] And NVIDIA is evaluating that node for a future design.[^intc-nvidia-18a-20260619] No order yet. But the whole Intel thesis comes down to whether anyone outside Intel will manufacture on its leading node — and NVIDIA kicking the tires is the first real evidence in years.Ava: And one to file away for the fall. Vertex got its kidney-disease drug, povetacicept, accepted for FDA review this week — its first real move into a major indication beyond cystic fibrosis, with a decision due November 30.[^vrtx-povetacicept-20260619] Not a Monday catalyst. But a real one on the calendar.CloseAva: That’s the show. Wall Street’s consensus on Micron heading into Wednesday: 30 analysts, unanimous Buy, an average target around $1,015 on a stock that’s already there.[^mu-analyst-target-revisions-20260619] Consensus says the supercycle is priced in. Consensus has been wrong about memory at every single turn of this cycle. Hiring data this week from Talnexis — talnexis.com. The throughline one more time: the AI demand debate is over. Whether the supply chain can deliver — the lithography, the power, the memory — is the only question left, and Wednesday’s Micron print is the first real answer. Hunt, Jason, and Mike are back Wednesday on episode 2626, picking up whether proprietary data can actually be protected.[^ep-e2625b] Download the Cash Flow Memo at telltales.us. I’m Ava Cabot. Thanks for listening.Closing disclaimerAva: The views expressed on this podcast are the host alone and do not constitute an offer to sell or a recommendation to purchase, or a solicitation of an offer to buy any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the host nor any of their employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness, or completeness of this information. The host and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future, and may or may not hold positions in the securities mentioned.Sources* ASML Holding. (2026). Q1 2026 financial results [Press release]. https://www.asml.com/en/news/press-releases/2026/q1-2026-financial-results* Barchart. (2026). FedEx’s Q4 2026 earnings: What to expect. https://www.barchart.com/story/news/1533352/fedex-s-q4-2026-earnings-what-to-expect* Bernstein / CNBC. (2026, June 16). GE Vernova (GEV) quote and analyst coverage. CNBC. https://www.cnbc.com/quotes/GEV* Cheniere Energy. (2026). Corpus Christi liquefaction project. https://www.cheniere.com/about/where-we-work/ccl* FDA panel recommends Moderna’s mRNA flu shot for older adults. (2026). NBC News. https://www.nbcnews.com/health/health-news/fda-panel-recommends-modernas-mrna-flu-shot-older-adults-rcna350699* FedEx. (2026). FedEx Board of Directors approves spin-off of FedEx Freight [Investor news]. https://investors.fedex.com/news-and-events/investor-news/investor-news-details/2026/FedEx-Board-of-Directors-Approves-Spin-off-of-FedEx-Freight/default.aspx* FXLeaders. (2026, June 19). Micron earnings preview: MU stock faces key test as earnings approach. https://www.fxleaders.com/news/2026/06/19/micron-earnings-preview-mu-stock-faces-key-test-as-earnings-approach-after-strong-rally/* Micron sold out of 2026 HBM. (2026, June 19). Yahoo Finance. https://finance.yahoo.com/news/micron-sold-2026-hbm-us-231248051.html* Micron Technology (MU) price target. (2026, June 19). Yahoo Finance. https://finance.yahoo.com/markets/stocks/articles/micron-technology-mu-price-target-011038074.html* Micron Technology (MU) wins HBM4 for Nvidia Vera Rubin. (2026, June 19). Yahoo Finance. https://finance.yahoo.com/technology/ai/articles/micron-technology-mu-wins-hbm4-211205119.html* Micron Technology: HBM sold out for 2026 — Wall Street is still underpricing. (2026, June 19). Seeking Alpha. https://seekingalpha.com/article/4881338-micron-technology-hbm-sold-out-for-2026-wall-street-is-still-underpricing* Nike China guidance reset. (2026). AInvest. https://www.ainvest.com/news/nike-china-guidance-reset-term-pain-confirms-deep-rooted-inventory-demand-headwinds-2604/* Nike stock 2026: NKE turnaround analysis. (2026). Top1Markets. https://www.top1markets.com/news/nike-stock-2026-nke-turnaround-analysis-elliott-hill* Sabine Pass LNG expansion contract. (2026). Simply Wall St. https://simplywall.st/stocks/us/energy/nyse-lng/cheniere-energy/news/sabine-pass-lng-expansion-contract-might-change-the-case-for* STAT Times. (2026). FedEx to reduce cost by $1bn in FY2026; net income drops 5% in FY2025. https://www.stattimes.com/air-cargo/fedex-to-reduce-cost-by-1bn-in-fy2026-net-income-drops-5-in-fy2025-1355655* Supply Chain Dive. (2026). Nike’s $1.5B tariff hit and sourcing shift. https://www.supplychaindive.com/news/nike-1b-tariff-sourcing-price-hikes/752159/* The end of cheap memory: Why 2026 marks a structural shift in tech economics. (2026, June 19). Investing.com. https://www.investing.com/analysis/the-end-of-cheap-memory-why-2026-marks-a-structural-shift-in-tech-economics-200675634* The Register. (2026, June 17). Intel starts cooking up enhanced 18A-P silicon for would-be foundry customers. https://www.theregister.com/systems/2026/06/17/intel-starts-cooking-up-enhanced-18a-p-silicon-for-would-be-foundry-customers/5257487* Timothy Sykes. (2026, June 17). Moderna Inc. (MRNA) news. https://www.timothysykes.com/news/moderna-inc-mrna-news-2026_06_17/* US tells ASML it is concerned China may have top chip tool. (2026, June 19). Bloomberg. https://www.bloomberg.com/news/articles/2026-06-19/us-tells-asml-it-s-concerned-china-may-have-top-chip-tool* Utility Dive. (2026). GE Vernova bullish on electrical infrastructure as turbine backlog grows. https://www.utilitydive.com/news/ge-vernova-bullish-on-electrical-infrastructure-as-turbine-backlog-grows/803631/* Utility Dive. (2026). GE Vernova expects to end 2025 with an 80 GW gas turbine backlog that stretches into 2029. https://www.utilitydive.com/news/ge-vernova-expects-to-end-2025-with-an-80-gw-gas-turbine-backlog-that-stretches-into-2029/807662/* Vertex Pharmaceuticals. (2026). Vertex announces US FDA acceptance of biologics license application for povetacicept [Press release]. https://news.vrtx.com/news-releases/news-release-details/vertex-announces-us-fda-acceptance-biologics-license-application* Yahoo Finance. (2026). Intel bets on 18A, Xeon 6. https://finance.yahoo.com/sectors/technology/articles/intel-bets-18a-xeon-6-070403655.htmlInternal dataInternal data is provided on a best efforts basis.Forward earnings* FDX — FedEx, 2026-06-23 (Tuesday) AMC, fiscal Q4 2026. Consensus EPS 5.91 / revenue $24.04B. Earnings calendar.* MU — Micron, 2026-06-24 (Wednesday) AMC, fiscal Q3 2026. (Consensus columns unreliable this week; report date verified.) Earnings calendar.* NKE — Nike, 2026-06-30 (Tuesday) AMC, fiscal Q4 2026. Consensus EPS 0.11 / revenue $10.85B. Earnings calendar.Hiring intelligence (Talnexis)* MU — Micron #3 hiring floor (3,061 open roles, +181 in the 7-day window), detected 2026-06-19. Source: Talnexis hiring intelligence, https://www.talnexis.com/ This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com | 12m 32s | ||||||

| 6/20/26 |  The End of the Subsidized-Token Era | All three hosts in one room: a macro tour through oil, gas and a new Fed chair, then a deep dive on NVIDIA at $5 trillion, the software stack’s capex problem, and the Anthropic export-control fight that turns proprietary data into the next moat.The Cashflow MemoKey Takeaways* Macro (Hunt’s exhibits): Oil sits ~$80 heading toward $70 (vs $60 on its way to $50 when the Iran event started), with backwardation compressing to under $10; natural gas averages ~$3.50 across both ’26 and ’27. New Fed chair Kevin Warsh signaled aggressive balance-sheet runoff (~$750B/yr toward a target near $1.5T) and a possible bias to hike — a lot of paper for the market to absorb against a ~$1.5T deficit.* NVIDIA at ~$5T is turning into a value stock: free cash flow on a $200-250B run-rate by year-end (vs a record ~$160B). The bull case has shifted from the chip cycle to TAM expansion — server → rack → row → full reference data-center design, an x86-killer CPU, and direct buildouts for cash-rich non-hyperscalers like Eli Lilly (~$20B FCF), Exxon/Chevron, and Citadel — though AI capex at ~3% of GDP raises a law-of-large-numbers ceiling on incremental budget growth.* Software dispersion is about capex risk: Salesforce screens cheap at ~18x FCF because it owns its own data centers and will likely have to deploy GPUs (capex rising from ~zero), while ServiceNow trades >50x renting AWS; Snowflake stays cash-light on heavy SBC but saw NRR re-accelerate on ~30% revenue growth as its AI product (chat over enterprise data) ramps.* The Anthropic throughline: a cyber-capable model released to ~40 entities (JPMorgan et al.), Amazon/Jassy lobbying Washington for export controls, the guardrailed Fable version jailbroken within two days, and distillation risk from Tencent/Alibaba (~1 year behind). The hosts read Jassy’s move as AWS self-protection, not public spirit — AWS was almost certainly one of the 40.* AI economics as a J-curve, proprietary data as the new moat: OpenAI/Anthropic head public with no profits against massive compute rent; the tell to watch is the end of the subsidized-token era (Uber/Lyft tripled fares post-IPO once VC subsidies ended). Microsoft blocked Anthropic’s models internally after a ToS change let Anthropic capture and train on user prompts (i.e., customer code) — a breach of trust that makes walled-off hosting (Citadel on Google) the real battleground.Show Notes[00:00] Intro & this week’s Cash Flow Memo Mike sets up the episode and points listeners to the memo at telltales.us.[00:26] Exhibits A/B/C — Oil, Gas & the Fed Hunt’s five minutes: oil $80 toward $70 with backwardation under $10, nat gas ~$3.50 across ’26-’27, and new Fed chair Kevin Warsh signaling balance-sheet runoff and a possible hike bias.[04:37] Apple & Snap — foldables, camera AirPods, AR glasses Apple’s underwhelming conference (a 2028 foldable, AirPods with cameras) versus Snap’s see-through AR glasses and why Meta’s audio-only glasses are the best product today.[07:30] Why Amazon called Washington on Anthropic Anthropic’s cyber-capable model, the limited release to ~40 entities, and the hosts’ read that Jassy’s export-control push is AWS self-protection.[10:53] Jailbreaking the guardrails & the China distillation risk The Fable guardrailed version cracked in two days, and why Tencent/Alibaba stay roughly a year behind.[13:46] What is SpaceX worth? — AI’s J-curve to profits SpaceX public and +30%, OpenAI/Anthropic going public with no profits, and how to think about revenue growth that costs enormous compute.[15:44] The end of the subsidized-token era Jason’s Uber/Lyft analogy: cheap VC-funded tokens today, tripled rates after the IPO.[16:11] Microsoft’s per-seat agent bet Why fixed price-per-seat plus usage upside is the right model for a slow-moving enterprise base, and the job-displacement question.[18:54] Software dispersion — Salesforce, ServiceNow & Snowflake Salesforce at 18x FCF and a coming GPU capex bill, ServiceNow renting AWS, and Snowflake’s NRR re-acceleration.[21:34] Oracle, Broadcom & NVIDIA at $5 trillion Oracle and Broadcom’s pivots, then NVIDIA as a record-FCF value stock.[24:45] NVIDIA’s next TAM — racks, rows, x86 & selling direct From server to full reference data-center design, going after the x86 CPU market, and building private clouds for enterprises.[25:53] Healthcare & the cash-flow hunt — Lilly, Exxon/Chevron, Citadel NVIDIA chasing free-cash-flow-rich customers: Lilly’s walled-off AI buildout, oil majors, and Citadel’s Google deal.[29:48] Proprietary data as the new moat Microsoft blocks Anthropic’s models after a ToS change to capture and train on customer prompts — a breach of trust.[32:31] Next week & sign-off A teed-up deep dive on protecting proprietary data: defense versus offense, and whether anything can truly be walled off.If these conversations have earned a place in your week, send the show to one person who’d genuinely enjoy it. Download the Cash Flow Memo at telltales.us.Cashtags$AAPL $AMZN $AVGO $BABA $CRM $CVX $GOOGL $JPM $LLY $LYFT $META $MSFT $NOW $NVDA $ORCL $SNAP $SNOW $TSM $UBER $XOM This post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com | 35m 40s | ||||||

| 6/19/26 |  The One Week We Were All in the Same Room | For the first time in four years, there’s no new Telltales episode this week.The one week all three of us were finally in the same city — Hunt, Jason, and Mike, in one room in New York instead of scattered across two coasts — the recording gremlins picked their moment. The primary recording failed partway through. There’s a backup, and we’re actively working to recover it.So here’s the plan: if we recover the audio, this week’s episode lands in your feed the moment it’s clean. If we don’t, no harm done — Hunt, Jason, and Mike are back in the chair next Wednesday, and Ava is back with the Weekend Update on Saturday.While you wait, this week’s Cash Flow Memo is below. And if these conversations have earned a place in your week, send the show to one person who’d genuinely enjoy it. Almost all of our growth has come from listeners doing exactly that — and we don’t take a single recommendation for granted.This post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.The Cashflow Memo This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com | 0m 58s | ||||||

| 6/15/26 |  Weekend Update - W2624 | ▶ Explore this week’s Tape — live, sortable, drill-down →Good News, Sold: The AI Buildout’s First Bill Came DueEvery capital cycle has the same tell. It is not the day the spending stops. It is the day the market stops clapping for it — when a company does exactly what it promised and the stock falls anyway. This week the most expensive trade on earth hit that day three times.Oracle delivered the backlog it told everyone it would deliver. A six-hundred-thirty-eight-billion-dollar pile of contracted future revenue, up more than three-and-a-half times in a year.¹ Cloud infrastructure revenue up ninety-three percent.² It did the thing. The stock fell ten percent.³For two years the AI trade was a referendum on demand: is it real, how big, how fast. The bull won that argument. So the market moved the goalposts, the way it always does at this point in a buildout — from is the demand there to who pays to meet it, and what does the bill do to the balance sheet carrying it. Bill Maris said the quiet part on All-In this week: a trillion dollars of spend commitments sitting on sixty billion of revenue, and now you go to the public markets and hope retail picks up the difference.⁴ That is the bear case in one sentence. Three names walked straight into it this week, and the interesting part is that each of them is paying the bill a different way.Oracle is borrowing it. Trailing free cash flow is already negative — they spent the better part of fifty billion dollars on capex to build the capacity behind that backlog, and the money to fund the next leg is coming out of the debt market into a tape that has stopped rewarding capital plans.⁵ NextEra is diluting for it. The biggest bet in the history of regulated utilities — a sixty-seven-billion-dollar, all-stock takeover of Dominion, built explicitly to wire thirty gigawatts of data-center power by twenty-thirty-five, Google and Meta already signed.⁶ All-stock is the tell. A utility already carrying sixteen times debt to free cash flow cannot borrow its way to the biggest deal in its sector’s history, so it is paying with equity and handing the cost to the shareholder it already has.⁷ The stock fell nine percent.⁸ Micron is the one name pre-selling it: its entire next fiscal year of high-bandwidth memory is already spoken for, certified into Nvidia’s roadmap, the demand contracted before the capacity ships.⁹Three funding strategies — debt, equity, pre-sold demand — and one underlying wager: that AI demand is durable enough to convert all of it to cash before the interest comes due. The cashflow read is in Marcus’s column below; short version, two of these three have no multiple to quote because the denominator is still negative. Page one of the Cash Flow Memo this week is a capex ledger, not an earnings sheet.This is what the back half of a capital cycle looks like, and it rhymes. The railroads, the fiber glut, the shale decade — the capital cycle never turns when the building stops. It turns when the market stops paying for the announcement and starts pricing the lag between the spend and the cash. The demand did not get worse this week. The accounting for it did.The next data point is dated. Micron reports Wednesday the twenty-fourth.¹⁰ On the screen it trades at a hundred times trailing free cash flow, which sounds insane and tells you nothing — that is trough cash flow at the bottom of a memory cycle. Price it forward and consensus has it at a single-digit multiple of next year’s earnings,¹¹ with trailing cash flow already up more than five-fold off the low.¹² The test is not the headline print. It is whether the forward demand the whole buildout is leaning on shows up in one company’s order book. If Micron’s guide confirms, the bill looks affordable. If it wobbles, the cycle just got more expensive for all three.Wall Street’s consensus on the AI buildout: too crowded, too expensive, too late. The stocks fell this week not because the demand soured — because the market finally started counting the cost. That is not the top. That is the capital cycle clearing its throat.The Tape — W2624Universe of 94 cashflow-memo names, snap dates 2026-06-05 → 2026-06-15. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamHealthcare spent the week getting repriced by Washington, and the screens are tarring the whole sector with one brush. Regeneron is the name that brush gets wrong. It sits near the top of the board at 11.3x EV/FCF on an 8.8% free cash flow yield — cheaper than UnitedHealth, with no federal prosecutor auditing the numerator. That is the distinction the table cannot draw: UNH’s cash engine is the thing the DOJ is investigating; Regeneron’s is a drug franchise nobody has subpoenaed. Same sector, same de-rate, two completely different reasons for the cheap — one is cheap because the cash might be fiction, the other because it shares a GICS code with the one that might be. The test on the next print is whether biosimilar pressure on the franchise shows up in the cash line, or the de-rate was just guilt by association.Telltales Yield — Bottom 10This Week’s ReportersSector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps90 of 90 ranked-eligible names ranked. 0 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-06-15.csv. NTM growth from FMP analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoWhen Cheap Stopped Being SafeThe week being cheap stopped being safe, and the AI buildout kept spending anyway.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the universe of the Cash Flow Memo. About 13 minutes. No filler.Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode 2625.Chapter markers* Time | Segment* 0:15 | Cold open* 0:55 | Theme — the AI buildout’s bill: Oracle, NextEra, Micron* 5:10 | Deep dive — UnitedHealth vs CarMax* 9:25 | Rapid-fire — Moderna, Intel* 11:30 | Close + Consensus WatchFull transcriptOpening disclaimerAva: The following conversation is intended for informational purposes only. You should always do your own work to determine if an investment is suitable for you.Cold openAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack. We’re still early — this is a pilot, and we want to hear what’s working.Ava: Here’s the week. Being cheap stopped being safe. The cheapest large-cap in healthcare spent the week with a federal prosecutor at the door. The retail name everyone screens as cheap is being handed customers by a tariff. And while the market was busy repricing the cheap stuff, the most expensive trade on earth — the AI buildout — just kept writing bigger and bigger checks, and got punished for it anyway. On Wednesday’s main show, episode 2624, Hunt, Jason, and Mike worked through the economics of that buildout — the data centers, and the sheer physics of powering them.[^ep-e2624] We’re going to put the cashflow lens on the bill. Because this was the week the bill started showing up in three different places at once.Theme — the AI buildout’s billAva: Start with the most expensive trade in the market, because this week it got complicated. For two years the AI story was demand — is it real, how big, how fast. This week the question flipped to cost. Who delivers it, who powers it, and whose balance sheet carries it. And here’s the contrarian note hanging over the whole thing: as Bill Maris put it on All-In this week, quote, a trillion in spend commitments on $60 billion of revenue, and now you’re going to go to the public and hope that retail is going to pick that up.[^tp-maris-allin-20260609] Hold that thought. Because three companies just tested it.Ava: Start with Oracle, because it did exactly what it promised and got punished for it. It delivered the backlog it said it would — and the stock fell 10% anyway.[^orcl-stock-20260610] Page 2 of the memo: remaining performance obligations hit a record $638 billion, up 363% year over year.[^orcl-rpo-20260610] Cloud infrastructure revenue up 93%.[^orcl-oci-growth-20260610] They did the thing. Marcus — why did doing the thing get them sold?Marcus: Because the market stopped grading the backlog and started grading the bill. Oracle’s trailing free cash flow is negative — minus $21 billion[^memo-orcl-fcf-20260615] — because they spent $48 billion on capex over the last year to build the capacity behind that backlog.[^memo-orcl-capex-20260615] So there’s no multiple to quote. Don’t reach for one; it’s a negative number. What prices Oracle now is one question: does $638 billion of contracted intent convert to cash before the interest on the build eats them. They raised the capital plan into a tape that no longer claps for capital plans. Maris’s line is the bear case in one sentence — and Oracle just walked straight into it.Ava: So next door, the power bill. NextEra just made the biggest bet in the history of regulated utilities — and got the same treatment Oracle did. A $67 billion, all-stock takeover of Dominion Energy, the largest regulated-utility deal ever, built explicitly to power AI data centers — 30 GW of it by 2035, with Google and Meta already signed on.[^nee-dominion-acquisition-20260610][^nee-datacenters-expansion-20260615] The stock fell 9%.[^nee-stock-decline-20260610] Marcus, what does the grid cost?Marcus: It costs more than NextEra has. This is a utility that already carries 16x debt to free cash flow[^memo-nee-debtfcf-20260615] — and it’s buying the biggest deal in the sector’s history. They’re paying in stock, not debt, which is the tell: they’re funding the buildout by diluting, because the balance sheet can’t borrow its way there at 41x free cash flow.[^memo-nee-evfcf-20260615] The 9% drop isn’t the market rejecting data-center power. It’s the market asking who eats the cost of building it — and deciding, this week, that the answer is the existing shareholder.Ava: And the third bill is memory, where Wall Street has completely lost its composure. Micron, page 5, reports a week from Wednesday — and ahead of it, price targets went from $550 to $1,750 in a matter of days.[^mu-pt-raise-20260608][^mu-analyst-targets-20260610] Micron got certified for Nvidia’s next-generation HBM4 memory, and its entire fiscal-year production is already spoken for.[^mu-hbm4-cert-20260610] One more tell you won’t see in the price: the Talnexis hiring tracker shows Micron added 200 roles last week, hiring at full-cycle pace.[^tlnx-mu-hiring-20260615] Marcus, the stock screens at 100x cash flow — is that insane?Marcus: It looks insane and it isn’t, and that’s the whole trick with memory. The 100x figure is trailing free cash flow at the bottom of the cycle[^memo-mu-evfcf-20260615] — it tells you nothing. Price it forward: consensus earnings put Micron at about 7x next fiscal year.[^mu-fwd-pe-20260615] Trailing cash flow is already up more than 5x off the trough, and revenue is guided to grow 60%+.[^memo-mu-fcf-20260615] You don’t value a cyclical on a trough multiple; you value it on where the cash is going — and forward, this is a single-digit multiple. The risk isn’t the price. The risk is that the whole supercycle thesis — Oracle’s backlog, NextEra’s gigawatts, Micron’s HBM — is one connected bet that the AI demand is durable. Three names, one wager. The print on the 24th is the next data point on whether it holds.Deep dive — UnitedHealth vs CarMaxAva: Now the other half of the market — the cheap half. Two companies, both trading at single-digit-ish multiples, both cheap for a reason, and the reasons could not be more opposite. One is being investigated by the government for charging too much. The other is being handed customers by the government’s tariffs. Same week, two service businesses, two completely different verdicts on what cheap means.Ava: Here are the headlines, side by side. UnitedHealth, all the way back on page 19 of the memo: the CEO, Andrew Witty, resigned; the company pulled its full-year guidance; and the Justice Department opened a criminal and civil probe into whether it inflated Medicare diagnoses to juice reimbursements.[^unh-ceo-resignation-20260615][^unh-guidance-pull-20260615][^unh-doj-probe-20260615] The stock is down about a third from its high.[^unh-stock-recovery-20260615] And CarMax, page 8, reports Wednesday — first print under a new CEO, with an activist on the register, into a tariff backdrop that’s pushing buyers out of new cars and straight onto its lots.[^kmx-cfo-transition-20260615][^kmx-activist-20260615][^kmx-tariffs-20260615] Marcus — which kind of cheap actually pays you?Marcus: Take the scary one first. UnitedHealth trades at 14x trailing free cash flow, a 7% yield.[^memo-unh-evfcf-20260615] On the screen that’s the cheapest quality compounder in the market. Here’s the problem: the thing generating the cash is exactly what the DOJ is investigating. The free cash flow comes from Medicare Advantage billing, and a federal prosecutor is now asking whether that billing was fraudulent.[^unh-doj-probe-20260615] So you’re not buying 14x earnings. You’re buying 14x a number that’s under subpoena. Cheap doesn’t help you when the regulator is auditing the numerator.Ava: And yet the stock just rebounded almost back to its high. Make that make sense.Marcus: It doesn’t, and that’s the tell. In the same two weeks the probe widened, six different shops raised their price targets — and Bank of America went the other way and cut it to neutral.[^unh-analyst-upgrade-20260615][^unh-bofa-downgrade-20260615] So the sell-side is openly split on the same name in the same fortnight. That’s not a market pricing a verdict. It’s a market pricing a coin flip on whether a federal probe breaks the cash engine or just dents it. When the analysts can’t agree which, the multiple isn’t cheap — it’s unresolved.Ava: So UnitedHealth’s cheap is a question mark. What’s CarMax’s cheap?Marcus: Cheaper on the screen than in the business. Price CarMax on earnings and it’s a mid-teens multiple — about 15x forward,[^kmx-fwd-pe-20260615] a normal retailer, not a coiled spring. So the bet was never the multiple. It’s the setup: tariffs added thousands of dollars to new-car prices, used demand is the spillover, and there’s an activist pushing the new CEO to convert it.[^kmx-tariffs-20260615] The test on Wednesday is one number — used unit volume. If that’s accelerating, the multiple re-rates. If it’s flat, it’s just a tired retailer at 15x.Ava: So one cheap stock where the earnings might be fiction, and one that’s barely cheap once you do the math. Marcus, ever the optimist.Marcus: I deal in denominators. But the asymmetry is real: UnitedHealth’s downside is a business model the government breaks; CarMax’s downside is a soft quarter. One is binary. The other is just cyclical. Same word — cheap — two completely different bets.Ava: Mark the calendar. Wednesday tells us which one.Rapid-fireAva: Two more to close, both moving fast.Ava: Moderna got a different kind of government attention — the bad kind. Health and Human Services terminated a $590 million contract for Moderna’s bird-flu vaccine, and cancelled 22 more mRNA research contracts across the board, under the new RFK Jr. vaccine policy.[^mrna-barda-birdfly-20260610][^mrna-barda-platform-shift-20260610] There’s an FDA advisory meeting Wednesday on an mRNA flu shot.[^mrna-fda-advisory-20260618] This is the same theme as UnitedHealth from the other direction — Washington isn’t just regulating healthcare this year, it’s picking which platforms live. mRNA just got told it’s on the wrong list.Ava: And Intel — remember Intel? Up 250% this year, and almost nobody noticed.[^intc-ytdperformance-20260615] The catalyst this week: Google committed more than 3 million of its TPU chips to Intel’s foundry for 2028, pulling that order away from Taiwan Semi.[^intc-google-tpu-20260608] Bank of America double-upgraded the stock straight from sell to buy.[^intc-bofaupgrade-20260611] After a decade of being the company the buildout left behind, Intel spent this week being the company the buildout came back to.CloseAva: That’s the show. Wall Street’s consensus this week: UnitedHealth is a falling knife, and the AI infrastructure names are crowded. One of those is wrong, and it’s the one nobody wants to touch. Here’s the throughline into Monday: being cheap stopped being safe this week, because the thing setting the price wasn’t the business — it was the government on one side and the buildout’s bill on the other. UnitedHealth at 14x with a prosecutor. CarMax at mid-teens with a tariff at its back. Oracle, NextEra, and Micron spending into the doubt. Cheap got cheaper, expensive kept spending, and the market spent the week deciding it doesn’t trust either one. The hiring data we cited on Micron is from Talnexis — talnexis.com. You can pull up the Cash Flow Memo yourself at telltales.us. The forward week is loaded: CarMax reports Wednesday, FedEx the following Tuesday in its first quarter as a pure-play after spinning off freight,[^earn-fdx] and Micron Wednesday the 24th.[^earn-mu] And Hunt, Jason, and Mike are back Wednesday on episode 2625. We’ll see you next Saturday.Closing disclaimerAva: The views expressed on this podcast are the host alone and do not constitute an offer to sell or a recommendation to purchase, or a solicitation of an offer to buy any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the host nor any of their employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness, or completeness of this information. The host and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future, and may or may not hold positions in the securities mentioned.Sources* Applied Clinical Trials Online. (2026, June). HHS cancellation of BARDA mRNA vaccine trial. https://www.appliedclinicaltrialsonline.com/view/hhs-cancellation-barda-mrna-vaccine-trial-design-oversight-funding* Bank of America via TipRanks. (2026, June). UnitedHealth downgraded to Neutral at BofA amid Medicare Advantage uncertainty. https://www.tipranks.com/news/the-fly/unitedhealth-downgraded-to-neutral-at-bofa-amid-ma-uncertainty* Converge Digest. (2026, June 10). Oracle’s AI infrastructure business drives 93% IaaS growth. https://convergedigest.com/oracles-ai-infrastructure-business-drives-93-iaas-growth/* Cryptonomist. (2026, June 4). UnitedHealth stock stalls near $377 as lawsuit risk returns. https://en.cryptonomist.ch/2026/06/04/unitedhealth-stock-stalls-near-377-as-lawsuit-risk-returns/* eciks.org. (2026, June 10). NextEra Energy to acquire Dominion Energy in $67 billion all-stock transaction. https://eciks.org/8282-85162-dominion-energy-nextera-67-billion-merger* eMarketer. (2026, June). Auto tariffs are an opportunity for used car dealers. https://www.emarketer.com/content/auto-tariffs-opportunity-used-car-dealers* Fierce Healthcare. (2026, June). DOJ’s criminal probe into UnitedHealth extends to Optum Rx. https://www.fiercehealthcare.com/payers/wsj-report-doj-interviewing-former-employees-about-medicare-billing-practices-unitedhealth* GuruFocus. (2026, June 10). NextEra Energy (NEE) shares decline amid Dominion Energy acquisition. https://www.gurufocus.com/news/8910473/nextera-energy-nee-shares-decline-amid-dominion-energy-acquisition* HeyGo Trade. (2026, June). Intel up 250% in 2026: Is the AI comeback real or a short squeeze? https://www.heygotrade.com/en/blog/intel-stock-2026-ai-comeback/* IndMoney. (2026, June 10). Oracle Q4 FY2026 earnings: Why ORCL stock fell 10% despite a strong beat. https://www.indmoney.com/blog/us-stocks/oracle-q4-fy-2026-earnings-orcl-stock-drop* Interactive Crypto. (2026, June 9). Micron jumps as HBM4 certification and a Wells Fargo $1,220 target reset the narrative. https://www.interactivecrypto.com/micron-jumps-9-9-as-hbm4-certification-and-a-wells-fargo-1-220-target-reset-the-narrative-jun-20* Maris, B. (2026, June 9). Bill Maris: How Google could crush AI competitors, why small funds win, and AI’s Atari stage [Video]. All-In Podcast, YouTube. https://www.youtube.com/watch?v=0umrMuUClC4* MEXC Learn. (2026, May 27–June 8). Wall Street upgraded UNH six times in two weeks (JPMorgan $466, Bernstein $492). https://www.mexc.com/learn/article/wall-street-upgraded-unh-six-times-in-two-weeks-can-unitedhealth-stock-hit-492-unh-price-target-2026-2030/1* The Motley Fool. (2026, June 10). Oracle just revealed a massive $638 billion backlog. Here’s why the stock fell anyway. https://www.fool.com/investing/2026/06/10/oracle-just-revealed-a-massive-638-billion-backlog/* PharmAphorum. (2026, June). UnitedHealth CEO Andrew Witty steps down. https://pharmaphorum.com/news/unitedhealth-ceo-andrew-witty-steps-down* Simply Wall St News. (2026, June). Why CarMax (KMX) is up 8.1% after rising optimism around its 2026 earnings report. https://simplywall.st/stocks/us/retail/nyse-kmx/carmax/news/why-carmax-kmx-is-up-81-after-rising-optimism-around-its-202* TheStreet. (2026, June). Intel stock: BofA raises price target to $135 | INTC. https://www.thestreet.com/investing/stocks/intc-intel-stock-price-target-bank-of-america-june-2026* Timothy Sykes News. (2026, June). CarMax (KMX) draws activist interest as traders eye earnings. https://www.timothysykes.com/news/carmax-inc-kmx-news-2026_06_03/* U.S. Food and Drug Administration. (2026, June 18). Vaccines and Related Biological Products Advisory Committee June 18, 2026 meeting announcement. https://www.fda.gov/advisory-committees/advisory-committee-calendar/vaccines-and-related-biological-products-advisory-committee-june-18-2026-meeting-announcement* U.S. Securities and Exchange Commission. (2026). UnitedHealth Group, Form 8-K, Q1 2026. https://www.sec.gov/* Vantage Markets. (2026, June 9). Intel stock up 11%: INTC jumps on Google’s 3M AI chip deal. https://www.vantagemarkets.com/market-analysis/intel-stock-price-analysis-june-9-2026/* Yahoo Finance. (2026, June). NextEra (NEE) anticipates adding up to 30 gigawatts of power for data centers by 2035. https://finance.yahoo.com/news/nextera-nee-anticipates-adding-30-104711159.htmlHiring intelligence* Talnexis. (2026, June 15). Hiring intelligence — Micron (200 new roles in 7 days, #9 hiring-velocity mover). https://www.talnexis.com/Internal dataInternal data is provided on a best efforts basis.Forward earnings (FMP)* KMX — 2026-06-17 (Wednesday), Q1 FY27. FMP /stable/earnings?symbol=KMX, pulled 2026-06-15.* FDX — 2026-06-23 (Tuesday), Q4 FY26 (first pure-play print post freight spin-off). FMP /stable/earnings?symbol=FDX, pulled 2026-06-15.* MU — 2026-06-24 (Wednesday), Q3 FY26, consensus EPS $19.96 / revenue $34.72B. FMP /stable/earnings?symbol=MU, pulled 2026-06-15.* MU forward P/E ≈6.9x — FY ending 2027-08-28 consensus EPS $108.83 (21 analysts) vs price $746.79. FMP analyst estimates (annual), pulled 2026-06-15.* KMX forward P/E ≈15x — FY ending 2027-02-28 EPS $2.35 (17.2x) / FY 2028-02-28 EPS $2.85 (14.2x) vs price $40.34. FMP analyst estimates (annual), pulled 2026-06-15. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com | 11m 16s | ||||||

| 6/10/26 |  Data Centers in Space: How SpaceX Justifies $2 Trillion✨ | oil marketUS-Iran standoff+4 | JasonMike | SpaceXTesla+1 | USIran+1 | oil marketSpaceX+5 | — | 27m 31s | |

| 6/6/26 |  Weekend Update - W2623✨ | AI fundingcapital spending+3 | — | AlphabetBerkshire Hathaway+4 | — | equitycash flow+3 | — | 12m 22s | |

| 6/3/26 |  The Greatest Insurance Business Ever Built, and Why It's Bankrupting Us✨ | insurancehealthcare+4 | — | Top Mark CapitalAmazon+4 | IranStrait of Hormuz+5 | insurance businessoil supply+5 | — | 36m 20s | |

| 5/30/26 |  Weekend Update - W2622✨ | market valuationmemory companies+3 | — | MicronSpaceX | — | trillion-dollar valuationMicron+5 | — | 9m 59s | |

| 5/27/26 |  How Do You Get to $2 Trillion?✨ | SpaceX valuationAI technology+3 | JasonMike | StarlinkStarship+9 | — | SpaceXvaluation+7 | — | 33m 35s | |

| 5/23/26 |  Weekend Update - W2621✨ | Capital structureNvidia+4 | — | NvidiaNextEra+12 | — | NvidiaCash Flow Memo+5 | — | 12m 31s | |

| 5/20/26 |  Google's Real AI Risk Isn't Just ChatGPT✨ | AI risksGoogle's business model+4 | Hunt LawrenceMike Nicoletti+1 | GoogleSaudi Aramco+6 | Red SeaOman+3 | AIGoogle+5 | — | 32m 11s | |

| 5/16/26 |  Weekend Update - W2620✨ | Earnings WeekMarket Analysis+4 | — | NvidiaEQT+6 | Big-Box | EarningsNvidia+5 | — | 11m 30s | |

| 5/13/26 |  "Senator, We Run Ads": Inside Meta's AI Cash Machine✨ | Meta's AI profitabilityoil market analysis+3 | — | Access-for-All programMeta+6 | IranStrait of Hormuz | MetaAI cash machine+7 | — | 35m 03s | |

| 5/11/26 |  Weekend Update - W2619✨ | Cashflow Memosupplier payments+4 | — | MicronAMD+9 | — | cashflowMicron+7 | — | 14m 45s | |

| 5/6/26 |  Hyperscaler Stack Decoded (e2619)✨ | hyperscalersAI buildout+4 | — | AmazonMicrosoft+3 | IranHormuz+1 | hyperscalersAI+7 | — | 34m 17s | |

| 5/2/26 |  Weekend Update — W2618✨ | capital cycle resetscloud margin stories+3 | Marcus Graham | AppleMeta+6 | — | cash flowinvestment+3 | — | 17m 41s | |

| 4/29/26 |  Why Costco Is the Most Challenged Big Retailer at 47x Earnings✨ | retail competitionoil market analysis+4 | — | F-35drones+5 | Strait of HormuzUS+1 | CostcoAmazon+7 | — | 34m 39s | |

| 4/27/26 |  Weekend Update — W2617✨ | Q1 financial resultsstock market analysis+4 | Marcus Graham | IntelCharter+9 | — | financial resultsIntel+7 | — | 12m 29s | |

| 4/22/26 |  Could Apple Be the Next Intel? (e2617)✨ | Apple's AI strategyCEO succession+3 | — | AppleCDC+3 | Strait of HormuzIran | AppleAI strategy+6 | — | 35m 28s | |

| 4/20/26 |  Telltales Weekend Update (Pilot W2616)✨ | earnings seasonAI technology+3 | — | Taiwan SemiASML+4 | — | earningsAI+3 | — | 10m 22s | |

| 4/15/26 |  Is Microsoft the Next Intel — or the OS for AI Agents? (e2616)✨ | MicrosoftIntel comparison+4 | — | MicrosoftIntel+6 | IranStraits+5 | MicrosoftIntel+7 | — | 34m 04s | |

| 4/8/26 |  From Bankruptcy to $100B FCF (e2615)✨ | NVIDIAbankruptcy+5 | — | NVIDIAEli Lilly+5 | — | NVIDIAEli Lilly+6 | — | 30m 45s | |

| 4/1/26 |  Apple at 50, Oil at a Crossroads (e2614)✨ | geopoliticstechnology+4 | — | Top Mark Capital | IranStrait of Hormuz+1 | oil pricesgeopolitical risk+5 | — | 35m 14s | |

| 3/25/26 |  From Oil Risk Premiums to Cancer Vaccines (e2613)✨ | energy outlookoil pricing+4 | — | IranUS+6 | — | oil risk premiumnatural gas pricing+5 | — | 34m 35s | |

| 3/18/26 |  20 Million Barrels and No Way Out (e2612)✨ | global energy marketsoil prices+4 | — | crudenatural gas | IranSaudi+3 | Strait of Hormuzoil market+5 | — | 33m 27s | |

Showing 25 of 281

Sponsor Intelligence

Sign in to see which brands sponsor this podcast, their ad offers, and promo codes.

Chart Positions

1 placement across 1 market.

Chart Positions

1 placement across 1 market.