Insights from recent episode analysis

Audience Interest

Podcast Focus

Publishing Consistency

Platform Reach

Insights are generated by CastFox AI using publicly available data, episode content, and proprietary models.

Total monthly reach

Estimated from 6 chart positions in 6 markets.

By chart position

- 🇳🇿NZ · Investing#853K to 10K

- 🇭🇺HU · Investing#121500 to 3K

- 🇨🇿CZ · Investing#132500 to 3K

- 🇦🇹AT · Investing#169500 to 3K

- 🇧🇪BE · Investing#187500 to 3K

- Per-Episode Audience

Est. listeners per new episode within ~30 days

1.6K to 7.5K🎙 Daily cadence·60 episodes·Last published today - Monthly Reach

Unique listeners across all episodes (30 days)

5.5K to 25K🇳🇿40%🇭🇺12%🇨🇿12%+3 more - Active Followers

Loyal subscribers who consistently listen

2.2K to 10K

Market Insights

Platform Distribution

Reach across major podcast platforms, updated hourly

Total Followers

—

Total Plays

—

Total Reviews

—

* Data sourced directly from platform APIs and aggregated hourly across all major podcast directories.

On the show

Recent episodes

Drill Baby Drill | Josh Young

May 15, 2026

52m 00s

Markets are Broken | George Robertson

May 11, 2026

59m 25s

Got Energy? | Matt Polyak, Hummingbird Capital

May 8, 2026

45m 59s

Nobody Special | David Nicoski | Bob Coleman | Zach Marx.

May 4, 2026

1h 33m 33s

This is the most OUTRAGEOUS deal I've seen in my 45 years on Wall Street

Apr 29, 2026

1m 24s

Social Links & Contact

Official channels & resources

Official Website

Login

RSS Feed

Login

| Date | Episode | Description | Length | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 5/15/26 |  Drill Baby Drill | Josh Young | 1. Strategic Actions and Decisions* Prepare for Persistent High Prices: Underwrite investments for a scenario where oil prices remain high for 18 months or more due to record inventory draws, even if the Strait of Hormuz reopens tomorrow. Supply normalization will take 3-6 months, but inventory normalization will take significantly longer. [04:35]* Ignore the “Super Glut” Narrative: Discard consensus forecasts predicting a large oil surplus and price crash, as these models were fundamentally wrong in January and February 2026, showing no build. Base decisions on physical inventory data, not paper market narratives. [11:30]* Avoid “Safe” Passive Energy Exposure: Do not rely on broad energy ETFs (like XLE) for alpha, as they are dominated by overvalued majors (Exxon, Chevron) with different risk profiles. Instead, seek idiosyncratic, small-cap value in out-of-favor niches like services and small-cap E&Ps. [15:05]* Focus on U.S. Onshore Drillers: Prioritize capital allocation towards undervalued onshore drilling companies (specifically Ensign Drilling) trading at a significant discount to replacement cost and offering high free cash flow yields, as this subsector shows a clear inflection point that the broader market is missing. [16:58]* Follow the Capital Allocators: Monitor insider activity closely; specifically, follow the lead of self-made billionaires like Murray Edwards and Fairfax Holdings, who own nearly 50% of Ensign Drilling, signaling high conviction when management buys at current levels. [36:57]2. Executive SummaryDespite the Strait of Hormuz closure causing short-term panic, Josh Young argued that the fundamental oil market was already tight before the conflict, with no supply build in early 2026. Current high prices are sustainable due to record low inventories and declining U.S. shale productivity. The primary action is to allocate capital to onshore land drillers (specifically Ensign) trading at 25% of replacement cost with a ~25% free cash flow yield. The market mistakenly views rig count declines as bearish, ignoring that lower productivity now requires more rigs to maintain production. Key risks include political irrationality prolonging the Strait closure, but the reward asymmetry is high. Avoid major integrated oils and tankers; focus instead on small-cap E&Ps and drillers where volatility offers a margin of safety.3. Key Takeaways and Practical Lessons1. Inventory Levels Drive Price More Than Daily Supply: The market is underestimating how long prices will stay high because inventory normalization will take up to 18 months, resetting the global floor price permanently higher.* Practical Lesson: Monitor weekly inventory reports rather than daily news headlines; calculate the “days of supply” forward to gauge price duration rather than just the current price.2. Low Rig Counts Are a Bullish Signal, Not a Bearish One: The falling rig count has created a value trap narrative, but falling well productivity means producers need 25% more rigs just to stay flat, creating an imminent demand surge for drillers.* Practical Lesson: When analyzing cyclicals, calculate the “efficiency gap”—if productivity falls but output is flat, input demand (rigs) must eventually rise, creating a lagging buy signal.3. “Precisely Wrong” Models Create Opportunity: Consensus forecasts from the IEA and banks predicting a 4-5 million barrel build were wrong; relying on precise but inaccurate models leads to mispriced assets.* Practical Lesson: Favor “directionally right” over “precisely wrong.” Reject any forecast that projects specific surplus/deficit numbers beyond 3 months unless they explain the margin of error.*4. Passive Investing Ignores the Best Dislocations: Broad energy ETFs are dominated by two majors (Exxon/Chevron). The best value (25% free cash flow yields) is in small, illiquid names that passive funds ignore.* Practical Lesson: Screen for companies with a “double discount”—trading below replacement cost and offering a high free cash flow yield. This provides a margin of safety even if the cycle takes longer to turn.5. Volatility is the Entry Fee for Alpha: Absorbing the volatility of hated sectors (onshore drilling) is the mechanism for outperformance, similar to taking illiquidity risk in the Yale model.* Practical Lesson: Set a “volatility budget.” Add to positions on sharp drawdowns when the thesis (falling productivity, tight inventories) remains intact, using the market’s fear to lower your cost basis.Follow Josh Young here on X - @JoshYoungWatch on Youtube below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 52m 00s | ||||||

| 5/11/26 |  Markets are Broken | George Robertson | 1. Strategic Actions and Decisions* Recognize That Traditional Market Models Are Broken: Do not rely on PE ratios, CAPE, or historical frameworks for short-term moves; these tools have lost predictive power due to structural shifts in trading and volatility. [02:56]* Ignore Trump-Driven Volatility as a Trading Signal: Filter out daily political noise and social-media-driven commentary; the administration generates intraday volatility but offers no reliable institutional memory or predictive edge. [07:47]* Prepare for Discontinuous Price Jumps (Fusion Markets): Price discovery is suppressed, so expect infrequent but massive 25–40% market moves every ~3 years rather than gradual daily or weekly trends. [12:56]* Adopt a Defensive Capital Structure: Split capital into two buckets—core “safe” money held in cash and very low-risk instruments, and a smaller speculative bucket for high-conviction bets (e.g., puts on major banks). [41:50]* Hedge Long-Term “Safe” Holdings Against Catastrophic Risk: Even traditionally safe private-sector assets may be challenged in a crash; consider using options on money-center banks (Wells Fargo, JP Morgan) as a portfolio hedge. [42:43]2. Executive SummaryIn my discussion with George Robertson, a fellow veteran who started in 1981, we concluded that financial markets have lost true price discovery due to high-frequency quant trading, passive indexing, and the gutting of regulatory enforcement. George argues that traditional valuation tools no longer work for short-term forecasting, and that suppressed daily volatility stores energy for catastrophic “fusion” moves every few years. He views Trump as a volatility generator offering no trading signal, and believes the Fed’s power is overstated. George’s recommended defense: hold most assets in cash, and hedge long-term holdings with options on major banks like JP Morgan to prepare for a systemic reset.3. Key Takeaways and Practical Lessons1. Price Discovery Is Broken, Not Just Inefficient: Dominant quant funds and HFTs have created a single, managed market with no diversity of opinion, meaning today’s prices do not reflect true supply/demand signals.* Practical Lesson: Stop relying on daily or weekly price action for entry/exit signals; instead, focus on multi-year structural hedges and position sizing for rare, violent dislocations.2. Ignoring Trump Is a Superpower in This Regime: The administration is a volatility-generating machine with no day-to-day consistency; analyzing every tweet or policy threat leads to overtrading and emotional decisions.* Practical Lesson: Build an explicit “political noise filter” into your investment process—wait for confirmed policy actions, not headlines, before adjusting allocations.3. Legal Fraud Is Now Systemic Weakness: Weakened SEC, FTC, and Sherman Act enforcement mean that “technically legal but wrong” actions go unpunished, rewarding bad actors and distorting capital allocation.* Practical Lesson: Assume no regulatory backstop for fraudulent corporate behavior; perform your own forensic accounting and avoid companies where valuation depends on unverifiable future claims (e.g., self-driving AI).4. The Fed’s Power Is Overstated and Political: The central bank cannot control inflation or asset prices as much as believed; its role is increasingly to take blame while fiscal and political forces drive outcomes.* Practical Lesson: Do not build portfolios around predictions of Fed rate cuts or hikes—focus instead on balance sheet resilience and real-economy signals (e.g., loan growth, employment).5. Prepare for “Fusion” Crashes, Not Normal Corrections: Suppressed price discovery stores energy that will release in sudden, catastrophic moves (25–40% drawdowns) every few years, not in tradable 5–10% pullbacks.* Practical Lesson: Keep core wealth in very safe, liquid assets (cash, T-bills) and use non-correlated hedges (e.g., deep out-of-the-money puts on indices or major banks) sized for a 1–2% portfolio cost annually.Follow George on X here - @BickerinBrattleWatch on Youtube below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 59m 25s | ||||||

| 5/8/26 |  Got Energy? | Matt Polyak, Hummingbird Capital | 1. Strategic Actions and Decisions* Prioritize Stocks with Both AI and Energy Tailwinds: Focus on companies that benefit from both the AI data center buildout and energy supply tightness, such as Bloom Energy, Solaris, and Liberty Energy, which are securing 15-year infrastructure-style contracts. [16:12]* Monitor Offshore Services for Cyclical Upside: Position in offshore drilling and field services ahead of potential rig additions and pricing power, as utilization approaches 80%, but be aware these are sensitive to a quick geopolitical resolution. [36:07]* Consider Natural Gas and Pipelines for Income: Look at natural gas companies and pipeline stocks for double-digit free cash flow yields, particularly those levered to rising volumes from West Texas and data center power deals. [39:42]* Avoid Tankers and Refiners as Weapons of Choice: Given the supply disruption in the Middle East, avoid overcommitting to tankers and refiners, as their economics could normalize quickly if the Strait of Hormuz reopens. [41:36]* Increase Energy Sector Weighting Meaningfully: Investors should consider raising energy exposure to a low double-digit percentage of their portfolio, reflecting its 11-12% contribution to S&P 500 free cash flow, not just its 3-4% index weight. [44:03]2. Executive SummaryThe energy sector is at a historic inflection point driven by three forces: extreme underweight positioning (2.8% of benchmarks), the largest physical supply disruption in history (over 1 billion barrels lost), and a $2 trillion AI-driven capital expenditure wave into power infrastructure. Matt argues energy’s 3-4% S&P weighting severely misrepresents its 11-12% free cash flow contribution, which could reach 20% by decade’s end. While the near-term volatility is driven by Middle East tensions, the secular theme of AI data centers needing reliable, on-site power creates durable opportunities. The most attractive plays are those bridging AI and energy—companies offering “bring your own power” solutions with long-term contracts—while avoiding refiners and tankers that could normalize quickly.3. Key Takeaways and Practical Lessons1. Perception vs. Reality Creates the Biggest Mispricing: The market was max underweight energy (2.8% of benchmark) despite energy demand growing every year for 15 years and a structural AI tailwind approaching $2 trillion in capital.* Practical Lesson: Do not confuse Wall Street narratives (recession, excess supply) with physical reality (tight inventories, rising demand). Verify inventory and CapEx data before accepting consensus.2. Physical Supply Disruption is Worse than Markets Price: Over a billion barrels lost in 60 days, with NOV reporting 10,000 Middle East wells offline—3,000 may never return. Physical crude trades 20% above paper markets, with some spot barrels at $200-230.* Practical Lesson: When physical premiums decouple from futures, use that gap as a signal to add exposure, as paper markets often lag real-world shortages.3. Long-Term AI Energy Demand is Backwardated, Not Priced: The back end of the oil curve sits in high 60s/low60s/low70s, ignoring that hyperscalers are spending 25% of capital on AI power infrastructure and making free cash flow negative for the first time in decades.* Practical Lesson: Buy the back end of the curve or stocks with 10-15 year contracts when the forward strip is complacent; history shows such dislocations resolve upward.4. Bring Your Own Power is the New Thematic: Hyperscalers want unregulated, on-site island power in their parking lots to avoid utility interruption. Companies like Bloom Energy and Solaris are turning six-month jobs into 15-year joint ventures with investment-grade counterparties.* Practical Lesson: Look for historically commoditized businesses (e.g., pressure pumpers) now securing infrastructure-style contracts; these can re-rate from 3x to 15x free cash flow multiples.5. The Downside is Limited Even if Peace Breaks Out: If Hormuz opened tomorrow, oil likely settles in mid-to-high $80s—a higher-for-longer floor. Refiners and tankers would normalize quickly, but wells and LNG facilities will take a year or more to restore.* Practical Lesson: Separate your portfolio into quick fix (tankers, refiners) vs. slow fix (wells, LNG, power infrastructure) exposures. The latter offers asymmetric upside with a defended downside.Watch on Youtube Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 45m 59s | ||||||

| 5/4/26 |  Nobody Special | David Nicoski | Bob Coleman | Zach Marx. | 1. Strategic Actions and Decisions* Investigate Counterparty Risk in AI-Driven Lending: The failure of Community Bank and Trust (GA) due to an AI underwriting algorithm suggests a new class of operational risk. Audit any third-party AI vendors or automated loan origination systems for concentration risk and fraud vulnerability. [00:04:06]* Prepare for a Liquidity Squeeze in Hyperscalers: Free cash flow is evaporating at Meta and Amazon, forcing debt issuance while dollar shortages emerge globally. Reduce exposure to Mag7 equities that rely on continuous CapEx spending to sustain valuations, as the market may soon penalize cash incineration. [00:11:28]* Reallocate from Hyperscalers to Physical Enablers: Capital expenditure is flowing to engineering, construction, and electrical component stocks (PWR, ETN, WCC), which are outperforming the Mag7 by over 70% year-to-date. Rotate portfolio weight into industrial picks-and-shovels plays that benefit from AI buildout without balance sheet risk. [00:20:39]* Monitor Dollar Shortages for Gold Entry Point: The dollar cannot break 101, and central banks (Japan, UAE) are intervening, signaling potential dollar weakness. Initiate or add to gold and silver positions if the DXY breaks below 96, as sentiment in miners is at extreme lows (11.54 bullish percentile). [00:43:30]* Focus on Energy Service Companies Pivoting to Data Centers: Natural gas demand from AI is creating structural tailwinds. Focus on energy service companies transforming from pressure pumping to power providers for “behind-the-meter” data center electricity, rather than traditional oil tankers. [01:17:13]2. Executive SummaryThe discussion centers on the first “AI-induced bank failure” in Georgia, where executives used an algorithm to mass-produce SBA loans, resulting in a 50% capital loss with taxpayers on the hook for 75% of losses. Concurrently, Meta and Amazon are burning cash on AI CapEx so aggressively that free cash flow is nearly gone, forcing debt issuance. The panel recommends rotating out of hyperscalers and into the physical economy: engineering and construction stocks (up 70% year-to-date), memory chips (SanDisk signing five-year prepaid contracts), and energy infrastructure. A liquidity crisis is looming due to dollar shortages and rising bond yields (ten-year at one-year highs). Gold sentiment is in the “toilet” at the 11th percentile, presenting a favorable risk-reward entry, while energy remains critically underweighted at only 3-4% of the S&P 500 despite massive structural demand.3. Key Takeaways and Practical Lessons1. AI is a Double-Edged Sword for Financial Risk: The Georgia bank failure proves that AI underwriting without human oversight created catastrophic losses (50% of capital lost). Executives bragged on a podcast about replacing “banking relationships” with algorithms, leading to presumed fraud where fake companies got automatically approved for government-backed loans.* Practical Lesson: Require manual review of government-guaranteed loans (SBA and USDA) issued via AI. Ensure the 25% unguaranteed portion is not securitized into “SOUP” and sold to yield-chasing pensions, as happened with this bank.2. Free Cash Flow is the Only Truth in the AI Bubble: Hyperscalers are hiding debt via special purpose vehicles and shrinking free cash flow to service CapEx. Google inflated earnings via a change in the valuation of their Anthropic stake, and Meta issued another $25 billion in debt after reporting.* Practical Lesson: Ignore adjusted earnings. Screen for companies where operating cash flow is declining while capital expenditures are rising more than 30% year-over-year, and avoid those with negative tangible free cash flow.3. The Bottleneck is Physics, Not Chips: Data centers are being canceled due to grid transmission limits and public opposition (Virginia gigawatt project pulled by Brookfield). You cannot code your way around turbine blade production or water availability.* Practical Lesson: Invest in companies solving physical constraints: transformer manufacturers (Eaton), electrical parts distributors (Wesco), and natural gas turbine servicers, not the data center operators themselves.4. Local Inference is a Threat to Cloud AI: Running AI models locally on high-RAM hardware (Apple Mac Studios with 128-256GB) solves privacy and legal issues for finance, healthcare, and legal sectors, bypassing expensive cloud tokens where costs are rising.* Practical Lesson: Be cautious on cloud AI compute providers and consider hardware enablers that benefit from the shift to edge computing, as inference represents 80 to 85% of data center demand today.5. Commodity Currencies Signal a Shift to Hard Assets: The Australian Dollar and Brazilian Real are breaking out versus the USD, which is the first time since 2002 that every commodity-rich country’s currency is accelerating against the dollar. Gold sentiment has pulled back to the 11th percentile.* Practical Lesson: If the US dollar breaks below 96, increase allocation to gold miners and aluminum (which is blowing away S&P performance), as the “inflate or die” policy will struggle against inelastic demand for food and energy.Follow Nobody Special on X here - @JG_Nuke Follow David Nicoski on X here - @davevermilionFollow Bob Coleman on X here - @profitsplusidFollow Zach Marx on X here - @zmarx_the_spotWatch on youtube Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1h 33m 33s | ||||||

| 4/29/26 |  This is the most OUTRAGEOUS deal I've seen in my 45 years on Wall Street | SpaceX just disclosed Musk's new compensation package:He gets up to 200 million super-voting shares if SpaceX hits a $7.5 trillion valuation, establishes a permanent human settlement of at least ONE MILLION people on Mars, and deploys roughly 100 terawatts of space-based computing power.Let me put the 100 terawatts in perspective:The entire electricity generation capacity of the United States is around 1.2 terawatts. The comp plan asks Musk to build more than 80x America's entire power grid... in orbit.This is a science fiction screenplay that somehow landed in front of the SEC.But here's why it actually matters for your portfolio...The S-1 reportedly claims a $28.5 trillion total addressable market, with over 90 percent attributed to AI. CapeFearAdvisors flagged this one cleanly: when Palantir went public, it disclosed a $119 billion TAM and the SEC reviewed and accepted it.SpaceX is claiming a market roughly 240x BIGGER.Now let's talk about what is actually being sold here:Reported 2025 revenue is approximately $15.5 billion. Starlink delivers around $11 billion of that with healthy margins, and the launch business is genuinely dominant. The problem is xAI - the AI piece doing all the heavy lifting in the trillion-dollar valuation pitch.xAI generated just $210 million of revenue in the first 3 quarters of 2025 while burning through $9.5 billion in cash.Ben Brey and Rupert Mitchell - a former Fidelity portfolio manager and a former head of equity capital markets at Goldman and Citi between them - ran a serious discounted cash flow on the actual operating businesses and arrived at roughly $400 billion. Lawrence Fossi covered their work recently and the math holds up.The IPO is being marketed at $1.75 TRILLION.The gap between what these businesses support and what Musk is asking the public to pay is roughly $1.35 trillion of pure narrative.Then layer on what we just learned last week...The New York Times investigation revealed Musk personally borrowed $500 million from SpaceX between 2018 and 2020 at rates as low as 1%, while bank prime rates sat around 5%. The same SpaceX has been used to bail out SolarCity, prop up Tesla during cash crunches, and absorb xAI when the AI losses became unmanageable.This is the same playbook he's run for two decades.Use a privately controlled entity as a personal piggy bank, and when the bills come due, find new investors to absorb the losses.The IPO is structured to keep that game going FOREVER.The Texas reincorporation strips away Delaware's fiduciary protections. Controlled-company status on the Nasdaq eliminates independent board requirements. And retail is being offered up to 30% of the offering (3x the normal allocation) because the institutions who actually do the math are quietly stepping away.Here is the part that finishes the case for me:Roughly $40 billion of the IPO proceeds are already spoken for before a single dollar reaches operations. About $23 billion retires SpaceX debt. Another $17 billion retires the high-interest debt sitting on xAI and X.This raise is not funding the future. It's just plugging existing holes that retail investors will now own.In my 45 years I've never seen a deal where the comp hurdle is colonizing another planet.I've never seen a disclosed TAM that exceeds verified comparables by two orders of magnitude.I've never seen a company asking the public to fund the retirement of debt incurred by separate private entities controlled by the same individual.Every red flag I've watched precede a major bust over four decades is sitting in this prospectus, in plain sight.The Tesla mispricing is being repeated on a far larger scale.And this time the bag is being handed directly to retail.Don't be the one holding it. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1m 24s | ||||||

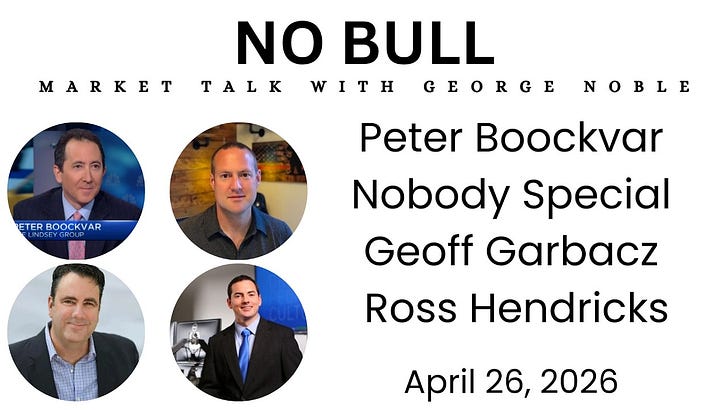

| 4/26/26 |  Peter Boockvar | Nobody Special | Geoff Garbacz | Ross Hendricks. | 1. Strategic Actions and Decisions* Reduce Exposure to Semiconductors Ahead of Hyperscaler Earnings: The AI trade is “completely splintered.” While semis are winning, the hyperscalers (Meta, Google) spending on them face deteriorating cash flows. If these companies announce they are “just maintaining” rather than increasing CapEx this week, it will be a “catalyst to sell off the semis.” [01:36]* Delay Any Investment in Small Modular Reactors (SMRs): Despite data center companies hinting at building their own power, “there is still not a single licensed small modular reactor design in the United States.” It remains “illegal to build any of them for power generation,” and NRC approval moves at the “speed of continental drift.” [04:02]* Prepare for a 60-70% Downside in Specific Semiconductor Names: One speaker explicitly states he expects his clients’ holdings in names like “Sanders” to “fall by 60, 70% before this is all over.” The cyclical nature of semis guarantees a major bust following the current boom. [13:00]* Rotate into Energy and Commodities on Pullbacks: Even if the Middle East war ends, “85 is the new 65” for oil. Global hoarding to refill strategic reserves and rework supply chains will create a “multi-year” bid under commodities. One speaker specifically likes “noble the driller and some natural gas companies.” [26:31]* Do Not Assume a V-Shaped Recovery or Fed Rescue: The post-GFC playbook of buying every dip is broken because central banks are in an inflationary world. Their “hands are tied” preventing the ability to cut rates or use QE to create a “V bottom” like in previous downturns. [01:00:17]2. Executive SummaryIn this recording, my guests and I broke down a market that is completely nonsensical right now. Peter explained how the AI tech trade has splintered, with semis exhibiting “1999-type behavior” while software falls through the floor. We warned that this is an extraordinarily cyclical group—big booms are always followed by major busts. Jack brought a critical on-the-ground reality check, highlighting how states like Wisconsin are forcing data centers to pay for their own grid upgrades, and noted that up to 40% of planned builds are already delayed. Geoff backed this up with short interest data showing semis at all-time highs with no covering pressure. Ross reinforced our commodity thesis, arguing that even if the war ends, oil’s floor is now $85. The through-line was clear: valuations don’t matter until they do, and the post-2008 “buy the dip” playbook is broken in today’s inflationary world. 3. Key Takeaways and Practical Lessons1. The “V-Bottom” Playbook is Obsolete in an Inflationary Regime: Investors trained to buy every dip assume infinite Fed stimulus. That era is over because central banks cannot cut rates or restart QE meaningfully with current inflation.* Practical Lesson: Do not assume a quick recovery in tech drawdowns. Supply-driven shocks require patience, not dip-buying heroics.2. Price-to-Sales Matters More Than P/E in Cyclical Peaks: Valuing a semi-company on one year of inflated earnings is a “mistake.” When gross margins are elevated but unsustainable, price-to-sales provides a clearer picture of risk.* Practical Lesson: Before buying a stock trading at 6x book, calculate its price-to-sales and compare it to historical norms, not just its low P/E ratio.3. Watch the Back End of the Oil Curve, Not the Front Month: Oil stocks did not rally as much as front-month crude because markets trade on long-term futures. The real move comes when back-end prices rise.* Practical Lesson: To enter a commodity trade, monitor the 12-36 month futures curve. A rising back end signals a structural shift, not just a geopolitical spike.4. Construction Logistics Are the Leading Indicator for Semis: The AI bottleneck is no longer chips; it is transformers, aluminum, and permits. Up to 40% of planned data centers are delayed for these reasons.* Practical Lesson: Monitor industrial construction metrics (transformer lead times, permitting rulings in states like Wisconsin) as the true leading indicator for semiconductor demand.5. Separate Technological Miracles from Business Viability: SpaceX is “freaking incredible” technologically, but its IPO valuation relies on a “self-referential” $28 trillion TAM cited by Elon Musk without evidence.* Practical Lesson: When evaluating IPOs like SpaceX, ignore the engineering superlatives and demand audited financials. If the TAM is self-reported by the CEO, treat it as marketing, not dataFollow Peter on X here - @pboockvarFollow Jack on X here - @JG_NukeFollow Geoff on X here - @bullet86Follow Ross on X here - @Ross__Hendricks Watch on Youtube below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1h 43m 22s | ||||||

| 4/19/26 |  Bring on the Liquidity | Nobody Special, Robert, Joe Carlasare | 1. Strategic Actions and Decisions* Monitor Hyperscaler CapEx for the Market’s “Reverse Gear”: The first major cut in capital expenditures by Microsoft, Amazon, Meta, or Google will likely end the current AI-driven rally. Jack argues this is the key signal to watch, as none of this has been priced in. [00:17:20]* Avoid Chasing Gold and Silver as Short-Term Trades: Do not buy precious metals while they are trading in lockstep with high-risk tech stocks. Jack notes that the same speculative money driving AI pumps is currently inflating gold, meaning a market correction will drag both down. [00:23:39]* Rotate Energy Holdings Away from Middle East Exposure: Focus on North and South American energy producers rather than global majors. Geopolitical instability and physical supply disruptions in the Strait of Hormuz make Middle East-exposed assets significantly riskier. [00:58:00]* Prepare for Middle East Sovereign Funds to Sell US Assets: GCC countries are likely to become net sellers of US stocks and bonds to fund war repairs and revenue shortfalls. This liquidity drain removes a key pillar of demand for the AI and data center buildout. [00:59:16]* Flag Flagstar Bank (NYCB) as a Systemic Risk: Flagstar Bank’s $14.6 billion exposure to NYC rent-controlled apartments is a ticking time bomb. A June 2026 vote on a rent freeze could trigger mass landlord defaults and reignite the regional banking crisis. [01:27:54]2. Executive Summary In this episode, I sit down with Jack, Robert, and Joe to dissect a market that is rallying on nothing but hot air. Jack and I see dangerous parallels to 1999 and 2021, pointing to AI pivots by failed companies and a $930 billion data center buildout with zero profits. Robert offers a contrarian view, bullish on TLT and long-term Treasuries, citing weak consumer growth and record short interest. Joe warns that domestic political instability and potential election disruptions are flying under the radar. Geopolitically, the Middle East conflict is strangling energy supplies, and I expect sovereign wealth funds to sell US assets, pulling the rug from under the AI bubble. While long-term bullish on gold due to fiscal deficits, I caution it is currently trading as a risk asset and will fall with tech in the short term.3. Key Takeaways and Practical Lessons1. Narratives are Liquidity, Not Truth: The market is trading false social media posts about peace as gospel, even when fighting resumes hours later. Fundamentals are irrelevant until the flows reverse.* Practical Lesson: Do not short a market just because the news is fake. Wait for a confirmed CapEx cut from a hyperscaler or a technical breakdown before acting.2. AI Has Generated No Profits, Only Losses: The $930 billion data center buildout has cost more than the US Interstate Highway System, yet the industry has not seen its first lick of profit. The only winners are hardware sellers.* Practical Lesson: Avoid any company that “pivots to AI” overnight. These are often the same scams from the 2021 cycle, such as MyKim (formerly Dat yet).3. Fragmentation is Inflationary: The weaponization of energy and breakdown of global supply chains will keep inflation structurally higher, regardless of Federal Reserve policy.* Practical Lesson: Hold gold and Bitcoin as long-term hedges, but buy them during risk-off sell-offs rather than chasing them during tech-driven rallies.4. The Commercial Real Estate Crisis Was Never Solved: The banking system simply papered over CRE losses with loan extensions and “extend and pretend.” Those loans are now maturing.* Practical Lesson: Watch Flagstar Bank closely. If NYC freezes rents in June 2026, expect a cascade of landlord defaults and potential regional bank failures.5. Negative Real Yields Make Hard Assets the Only Safe Haven: The US government cannot afford to let long bond yields spike given $40 trillion in debt. Financial repression or yield curve control is likely coming.* Practical Lesson: In a negative real yield environment, sell bonds into any rally caused by “growth scare” narratives and rotate into gold, silver, and Bitcoin.Follow Nobody Special on X here - @JG_NukeFollow Joe Carlasare on X here - @JoeCarlasareFollow Robert on X here - @infraa_Watch on Youtube Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1h 31m 30s | ||||||

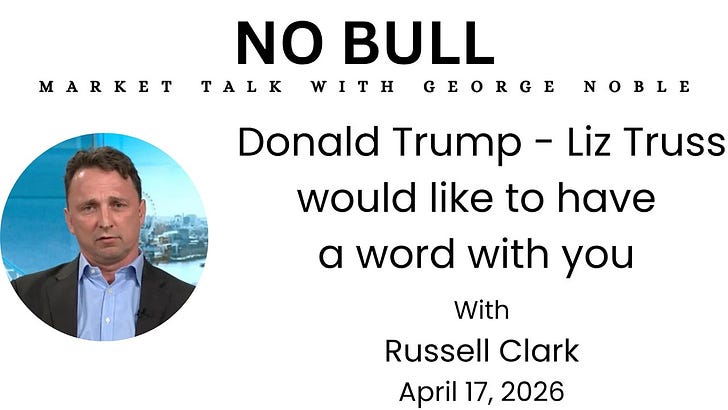

| 4/17/26 |  Donald Trump - Liz Truss would like to have a word with you | Russell Clark | 1. Strategic Actions and Decisions* Ignore Geopolitical Headlines and Focus on Structural Trends: The market can only focus on one thing at a time. Ignore the noise because “the real story” is the rising cost of capital. [00:28]* Avoid Crowded Shorts and Borrow Costs Above 2%: Never short “dream” stocks like Tesla. “If the borrow cost is over 2%, it’s not worth the short.” Crowded shorts create a situation where only buying is possible because long holders are locked up. [28:21]* Short Long-Dated Treasuries (TLT) as a Core Hedge: The primary risk is a spike in long-term bond yields. Use short TLT as a hedge because “if Treasury yields went to 10%, everything’s a short.” Wait for a big rebound to add to shorts rather than covering into a crash. [35:15]* Monitor Hedge Fund Basis Trades in Treasuries for a Liquidity Crisis: Foreign official buying of Treasuries has been replaced by hedge fund basis trades. “At some point, you’ll get a shock to the Treasury market... which then creates a margin call crisis,” similar to the UK gilt market in 2022. [38:35]* Maintain Long Gold (GLD) Against Short TLT, Not the Other Way Around: Most people view it as long gold hedged with short TLT, but the stronger view is to hate TLT. A Treasury crisis will force a central bank bailout, and “gold will explode because of the liquidity injection.” [44:05]2. Executive SummaryIn this episode, I sat down with my friend Russell Clark to cut through the geopolitical noise on Iran and oil. Clark argues the real story is structurally rising global capital costs driven by a political shift back toward labor. While wage inflation and fiscal spending have fueled equities, the government cannot tax enough, leaving a widening deficit. Foreigners no longer buy Treasuries willingly; hedge funds using leveraged basis trades have replaced them. Clark runs a paired trade: long gold (which he believes will benefit from a Fed bailout) hedged with short TLT (the trigger). He warns that private credit is mispricing assets like Japanese banks in the 1990s, and clearinghouse algorithms assume tomorrow looks like today, setting up a crash similar to the XIV volatility product or the Liz Truss gilt crisis.3. Key Takeaways and Practical Lessons1. Political Regime Change Drives Markets More Than Economics: The shift from the 1980s “low inflation” mandate to today’s pro-labor, pro-wage inflation mandate is the dominant force. “When the politics changes, markets change.” The Teamsters came out in massive support of Donald Trump.* Practical Lesson: “If you go read the Communist Manifesto... you learn a lot of interesting things.” The US growth model is now based on exploiting sovereign bond investors, and those investors are waking up.2. The Crowding Out Effect is Returning: Government borrowing is eating the pool of capital. “We’re getting close to the crowding out effect becoming a more overwhelming factor.” Corporate credit spreads are only tight because government bond yields are low.* Practical Lesson: If you are willing to lend to the US government at 4% for ten years with a 7% deficit, then corporate credit spreads are actually correct for where government bonds are.3. Central Clearing Creates Hidden Systemic Risk (The “Live Crash”): Post-GFC clearinghouses removed banks watching banks. “The fear of bankruptcy is what kept banks and traders honest.” Now algorithms assume liquidity today means liquidity tomorrow until a shock hits, then “the price falls more and more” in a doom loop.* Practical Lesson: “We saw this with the UK gilt market... XIV in 2018.” Both were resolved by central bank bailouts. When it happens in TLT, do not buy bonds; gold is the beneficiary of the liquidity injection.4. Private Equity and Private Credit are Marking Fantasy Prices: The industry operates on “I’ll buy yours if you buy mine,” similar to Japanese banks in the 1990s. When Shinsei Bank tried to mark loans at 60-80 cents on the dollar, bigger banks bought them at 100 cents to avoid taking losses on their own books.* Practical Lesson: “Rather than having third-party independent pricing of assets, we accepted ‘mark-to-magic.’” Avoid these structures because the self-interest to price correctly is not there.5. The AI Trade Will Not Stop for Valuations, Only for Bonds: Unlike the dot-com bust where corporates didn’t understand the internet, today’s tech giants know “investing through the downturn is how you succeed.” Microsoft, Google, Meta, and Amazon will not cut CapEx.* Practical Lesson: “The money is there until the bond markets say, ‘Hey, we can’t lend to you anymore.’” Do not short AI based on valuation. The only thing that stops CapEx is a Treasury market seizure.Watch on Youtube below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 54m 30s | ||||||

| 4/16/26 |  REMINDER: Live Zoom Call in 90 minutes | This is your reminder for the Noble Update LIVE Zoom call today at 2 PM EST.Join in, ask any questions you have, and get a no-BS answer from me.It’s been a wild week, and many people seem to be focusing on the wrong things — I’ve got plenty of value to add.Talk soon.(For paid subscribers only) This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 0m 47s | ||||||

| 4/12/26 |  Tacos, Sentiment and Seasonality | Jeff Hirsch | 1. Strategic Actions and Decisions* Monitor “Taco Trade” Technical Patterns: Track the specific March/April double-bottom pattern observed during the Trump presidency years, which historically precedes a bullish trend for the second and third quarters. [08:06]* Utilize Institutional Sentiment Benchmarks: Prioritize “Investors Intelligence” data over retail-focused surveys to gain a more robust understanding of where paid advisors and institutional money are positioned. [12:37]* Implement Seasonal Sector Rotations: Transition away from gold and technology as their primary bullish windows close, shifting focus toward defensive utilities and energy through the “worst six months” (May–October). [18:24]* De-risk AI and High-Beta Growth Exposure: Reduce positions in “hyperscalers” and software stocks (e.g., Microsoft, Oracle) due to deteriorating relative strength and a massive disconnect between capital expenditure and cash-on-cash returns. [41:24]* Diversify into International and Materials Sectors: Allocate capital toward outperforming non-U.S. markets like Brazil and specific industrial materials like aluminum and tungsten that are showing secular strength. [54:41]2. Executive SummaryIn this session of The Noble Update, I sat down with Jeff Hirsch to break down the treacherous seasonal waters ahead. We are entering the “worst six months” for equities, a period complicated by the midterm election cycle and persistent inflation. My primary concern remains the catastrophic capital destruction in the AI sector; I see a massive disconnect between the hundreds of billions being spent by hyperscalers and their actual cash returns—it’s dot-com 2.0 but with greater capital intensity. While Jeff looks for “Taco Trade” patterns, I am focused on the market’s internal rotation away from growth toward utilities, energy, and international value like Brazil to preserve capital.3. Key Takeaways and Practical Lessons1. The Four-Year Cycle Weak Spot is Imminent: The second and third quarters of a midterm election year historically represent the weakest period for the Dow and S&P 500.* Practical Lesson: Tighten stop-losses and limit new long positions in broad indices until the seasonal “best six months” resumes in October.2. Sentiment is a Trend, Not Just a Level: Market volatility (VIX) and sentiment readings are most predictive when analyzed as a trend of “higher lows” rather than static numbers.* Practical Lesson: Avoid “bottom-fishing” in tech stocks during a VIX uptrend; wait for a clear trend reversal in volatility before re-entering.3. The AI Capex Disconnect Signals a Bubble: High capital intensity without immediate return on investment (ROI) suggests a repeat of the 1999 fiber-optic build-out, where the technology succeeded but the stocks collapsed.* Practical Lesson: Stress-test growth holdings by demanding evidence of “cash-on-cash” returns rather than relying on thematic narratives or “use cases”.4. Utilities Serve as a Tactical Summer Hedge: Historically, utilities and bonds outperform during the market’s seasonally weak summer months.* Practical Lesson: Shift tactical allocations into the XLU (Utilities ETF) or companies involved in nuclear energy to maintain defensive yield.5. Global Relative Strength Favors Non-U.S. Equities: Markets like Brazil have significantly outperformed the S&P 500, signaling a breakdown in the U.S. dollar’s long-term uptrend.* Practical Lesson: Look beyond the S&P 500 for alpha by identifying markets that have broken multi-year secular downtrends, such as the Brazilian Real.Follow Jeffrey Here on X - @AlmanacTraderWatch on Youtube Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1h 02m 24s | ||||||

Want analysis for the episodes below?Free for Pro Submit a request, we'll have your selected episodes analyzed within an hour. Free, at no cost to you, for Pro users. | |||||||||

| 4/9/26 |  Keep it Real | David Nicoski, Vermilion Research | 1. Strategic Actions and Decisions* Prioritize Hard Assets with Low Obsolescence: Focus capital on securing positions in energy, materials, and real assets to mitigate risks from currency weakening and rising global nationalism. [00:15]* Monitor Internal Index Rotations: Avoid making generalized index calls and instead drill down into specific group outperformance, such as regional banks which have recently outperformed large caps by over 20%. [02:18]* Rotate Within Technology Verticals: Shift capital away from the “obliviation” occurring in software and toward resilient tech growth areas like broadband satellite, optical equipment, and lasers. [06:05]* Accumulate Commodities on Pullbacks: Utilize technical indicators like the RSI to identify overbought levels in sectors like energy and buy during weekly pullbacks to established support levels. [10:11]* Leverage Relative Strength in Global Markets: Execute trades in commodity-rich emerging markets like Brazil (EWZ), which are breaking 10-year base structures and outperforming the U.S. market significantly. [13:17]2. Executive SummaryI recently sat down with my long-time friend David Nicoski to dive into the charts, and his insights on this secular bull market in hard assets are something every leader needs to hear. Dave’s core thesis is that global nationalism and a decade of under-investment have made energy and materials the primary drivers of performance today. While we’re seeing “obliviation” in software, Dave pointed out that leadership still exists in tech if you look toward photonics and semiconductors. The big takeaway from our meeting is that the broad indices are a “fool’s errand”—success right now is about finding relative strength in specific niches like discount retail, meat production, and regional banks. We should prepare for continued outperformance in real assets as currency crosses shift toward commodity-producing nations.3. Key Takeaways and Practical Lessons1. Indexation Masks True Performance: Making generalized calls on market indices is a “fool’s errand” because the deviations between sectors are currently at historical extremes.* Practical Lesson: Analyze the “breadth” of sub-sector boxes—counting bullish versus bearish charts—rather than relying on headline index prices to determine the true health of a market segment.2. The “K-Shaped” Consumer Shift: High-end retail is currently being decimated, while discount retailers like Walmart and Costco maintain exceptional relative strength.* Practical Lesson: Monitor consumer staples and discount retailers as a defensive hedge, as they are capturing the “upper portion of the K” that is falling away from luxury brands.3. Long-Term Trend Breaks Overrule Short-Term Noise: Breaking a 10- or 15-year relative strength downtrend in commodities is a much more powerful signal than a minor two-week price correction.* Practical Lesson: Identify “ascending triangle” breakouts and multi-year base structures in materials like aluminum to capture secular, long-term gains rather than chasing daily volatility.4. Physical vs. Paper Market Divergence: The “paper” price of commodities, influenced by shorting and speculation, often fails to reflect the reality of physical supply shortages where buyers pay substantial premiums.* Practical Lesson: Watch for instances where physical buyers are willing to pay significant premiums over the “paper” price as a leading indicator for the next leg of a commodity rally.5. Nationalism Drives Supply Chain Security: Countries are increasingly focused on securing their own energy and material assets, creating a structural floor for commodity prices. * Practical Lesson: Allocate toward “commodity-rich” emerging markets like Brazil, where local currencies and equities are inflecting bullishly against the U.S. dollar.Follow David On X Here - @davevermilionWatch on Youtube Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 35m 26s | ||||||

| 4/6/26 |  $5 trillion in sovereign wealth is being rethought right now | Most investors have no idea what that means for their portfolios.Gulf sovereign wealth funds (Saudi Arabia's PIF, Abu Dhabi's ADIA, Qatar's QIA) collectively control roughly $5 trillion in global assets.They own stakes in Volkswagen, Barclays, Glencore, Harrods, the Shard, Heathrow Airport, and Canary Wharf. They're anchored across European blue chips, US Treasuries, Silicon Valley tech, and Manhattan real estate.These funds were built for a rainy day.And it's POURING.One month into the Iran war, the damage is adding up FAST. Saudi Arabia was forced to cut oil production from 10.4 million barrels per day in February to 8 million in March. At Brent above $110, that's over $8 billion in lost crude revenue in a single month. Add the shutdown of LPG terminals and surging insurance costs, and Saudi's total first month losses climb to roughly $10 billion.The UAE got hit differently. Not just oil disruption - Iran's drones struck data centers, ports, and aviation infrastructure. Dubai and Abu Dhabi built their global brand on logistics, tourism, and trade. All three are now under severe strain.Qatar may have it worst though.Its core LNG export infrastructure took direct hits. The $580 billion QIA owns trophy assets across Europe - 17% of Volkswagen, stakes in Barclays, Glencore, the London Stock Exchange, plus Harrods, Heathrow, and the Shard. If the conflict drags on, some of those crown jewels may need to become cash.3 of the 4 largest GCC economies have already BEGUN internal reviews of their investment strategies.They're reviewing existing contracts. Evaluating force majeure clauses. Reconsidering hundreds of billions in US investment pledges made to Trump just last year.Here's what I want you to understand:These funds don't just own stocks and buildings. They ARE the market in many corners of it. When the third largest shareholder in Volkswagen starts thinking about liquidity, that's a structural event - not just a portfolio adjustment.And the math is getting worse by the day.Saudi Arabia's 2026 budget was ALREADY built on a $44 billion deficit. Public debt was projected to hit $430 billion. Oil still accounts for 54% of state revenues. Every month this war continues forces Riyadh to choose between slowing Vision 2030 megaprojects or borrowing more on international markets.The good news (if you can call it that) is these funds hold significant liquid assets. ADIA reports 60-75% of its portfolio in public equities and debt. They can sell without fire-sale conditions.But "can sell" and "the market absorbs it smoothly" are two very different things.The IEA's Fatih Birol said last week that April will be MUCH worse than March for oil supply. The ships that were already in transit when the war started have now delivered. Nothing new is coming through Hormuz. The physical reality is catching up to paper prices.Brent is at $111 today. Goldman says $150-200 if the blockade persists through June. This is literally the worst energy disruption in history - bigger than '73, bigger than the Gulf War, bigger than the Russian gas cutoff.Meanwhile, gold sits at $4,675. Up over 25% since early 2025.The sovereign wealth fund story is the SECOND ORDER effect nobody's pricing in. Oil disruption is the headline. The possibility of $5 trillion in institutional capital being redeployed, liquidated, or frozen is the aftershock.When governments face existential short-term risk, long-term investment horizons collapse overnight.That's not theory. That's happening RIGHT NOW across the Gulf.Own gold. Own energy. Stay out of the way of forced sellers. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1m 16s | ||||||

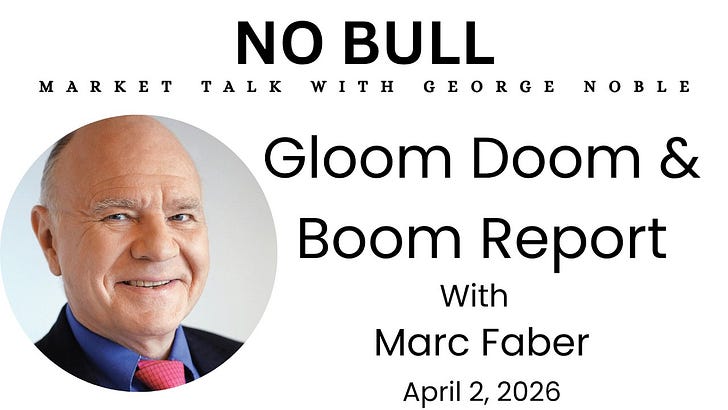

| 4/3/26 |  Gloom Doom & Boom Report | Marc Faber | 1. Strategic Actions and Decisions* Diversify across uncorrelated asset classes immediately: Own a mix of stocks, cash, bonds, real estate, and precious metals rather than trying to time or beat a rigged market. [03:16]* Admit ignorance and stop trying to forecast short-term moves: Accept that the future is unknowable; use broad diversification and value-based long-term positioning instead of momentum trading. [14:30]* Hold gold as insurance against central bank money printing: Treat gold not as an income-producing investment but as a policy hedge against the inevitability of currency debasement. [29:52]* Reduce or avoid long-dated U.S. bonds (TLT): Government balance sheets are insolvent, and bonds will likely destroy purchasing power in real terms despite nominal returns. [34:49]* Allocate capital to emerging economies, particularly Asia: Shift exposure away from overvalued U.S. markets toward Taiwan, South Korea, India, and other rapidly growing Asian economies. [44:12]2. Executive Summary In this conversation, my longtime friend Marc and I discussed a major market regime change away from the free-money era. We agreed the system is rigged—legal fraud, front-running, and fake inflation data are rampant. However, rather than rage against it, my advice to investors is to trade the market you have. Marc and I recommend diversifying across stocks, cash, real estate, and gold, while avoiding long-term bonds. We believe central banks have created illusory wealth and that the breakdown has already begun, evidenced by value outperforming growth last year. My key takeaway: own gold as insurance, invest in emerging economies, and accept modest real returns of 2-3%.3. Key Takeaways and Practical Lessons1. The System is Rigged—Accept It and Adapt: Legal fraud, front-running of retail orders by firms like Citadel, and manipulated inflation statistics mean the game is stacked against short-term traders.* Practical Lesson: Stop day trading and momentum speculation entirely. Shift to a long-term, value-oriented, diversified portfolio where micro-cheating by high-frequency firms does not matter.2. Diversification is the Only Honest Strategy for Non-Experts: Neither Marc nor I can predict the future—not in five minutes, not in five years. Admitting ignorance is the first step to rational investing.* Practical Lesson: Own at least five uncorrelated asset classes (stocks, cash, bonds, real estate, gold). Rebalance annually without trying to forecast which will outperform.3. Long Bonds are a Quiet Wealth Destroyer: Measuring bonds in dollars creates illusionary safety. When measured against gold or stable currencies, U.S. long bonds are in a multi-year bear market.* Practical Lesson: Replace long-duration Treasury holdings with gold or diversified emerging market equity exposure. If you must own bonds, keep maturities under five years.4. Gold is Insurance, Not an Investment: Gold produces no income, but its role is to protect against the inevitability of government money printing and the breakdown of paper currencies.* Practical Lesson: Allocate 10-15% of your portfolio to physical gold or GLD. Do not trade it. Hold it as catastrophe insurance against central bank stupidity.*5. The Old Rules of Valuation are Returning: The era of free money, chart momentum, and passive indexing is ending. Fundamentals—cash flow, debt levels, price-to-earnings—will matter again.* Practical Lesson: Write old-fashioned three- to four-page fundamental reports before buying any stock. Include strengths, weaknesses, risks, opportunities, valuations, financials, and catalysts. Ignore momentum alone.Visit Marc’s website here - https://www.gloomboomdoom.com/ Watch on Youtube Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 48m 09s | ||||||

| 4/2/26 |  Why Warren Buffett sits on $300 billion in cash | In a recent interview, Buffett was asked about the market selloff.His answer was devastating in its simplicity:"This is nothing."Markets are down 5-7% and everyone's panicking. Buffett has watched Berkshire drop 50% THREE times.He doesn't get excited about a 5-6% dip. In his own words: "We aren't in it to make 5 or 6 percent."These prices aren't even close to cheap.And the numbers back him up:Buffett's own favorite indicator - total market cap to GDP - is at 208%.He once called anything above 120% "playing with fire."We're nearly DOUBLE that threshold.At current levels, his model projects roughly 0.4% annual returns over the next 8 years.Zero point four percent.You can get 5% in a savings account.Meanwhile, Moody's AI-driven recession model just hit 49% probability. Every time it's crossed 50% in 80 years of backtesting, a recession followed within 12 months.And that reading was BEFORE the Iran war shut down the Strait of Hormuz and sent oil above $120.The IEA calls this the worst energy crisis in history. Worse than 1973. Worse than 1979. We've lost 12 million barrels per day - more than both 1970s oil crises COMBINED.The S&P is down 7% year to date. The Nasdaq is off 10%. Q1 was the worst quarterly performance in 4 years.US GDP growth just got revised down from 1.4% to 0.7%. The economy LOST 92,000 jobs last month when economists expected a GAIN of 59,000.And inflation is creeping higher while the economy slows.This is the early stage of stagflation.Buffett sees it. That's why he's been a NET SELLER of stocks for 9 straight quarters. That's why Berkshire is sitting on its largest cash pile in history.The greatest investor alive is telling you - not with words, but with actions - that this market is overpriced and he'd rather earn 5% in T-bills than own stocks at these valuations.When has Buffett been this cautious?Late 1999. Right before the dot-com crash wiped out 49%.Late 2007. Right before the financial crisis wiped out 57%.Both times he was mocked for "missing the rally."Both times he was right.Now look at what's happening around us:Oil at $120 with the Strait of Hormuz still closed. Gas above $4 for the first time since 2022. The IEA warns April will be WORSE than March.This is comparable to the 1970s stagflation era.And the market is still priced for perfection.Buffett didn't get rich by buying expensive stocks during geopolitical crises. He got rich by being patient, sitting in cash, and buying when everyone else was panicking.We're not at the panic stage yet.We're at the stage right before it.The smart money isn't buying this dip.The smart money IS the dip. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1m 02s | ||||||

| 4/1/26 |  Why is no one questioning this? | $315 BILLION in stablecoins are now backed by US Treasuries.And I don't understand why no one's questioning this.Goldman's David Solomon and former Treasury Secretary Steve Mnuchin just did a victory lap on stablecoins. Their pitch:Stablecoins strengthen the dollar, create demand for Treasuries, make it easier for people outside the United States to hold dollars.Sounds great. Until you look at what's actually happening underneath...The GENIUS Act passed in July 2025. First federal stablecoin framework in US history. Stablecoin market cap has grown 50% year over year. Tether alone holds $141 billion in US Treasuries, making it one of the largest holders of American government debt on the planet.Washington's pitch is simple: every time someone in Argentina, Turkey, or Nigeria buys USDT, they're buying Treasuries by proxy. Dollar dominance strengthened. Problem solved.And here's the part they REALLY love...The US ran an $1.8 trillion deficit in fiscal 2025. CBO projects $1.9 trillion this year. National debt just crossed $39 trillion. Interest payments alone now exceed $1 trillion annually. Meanwhile, the biggest foreign buyers of Treasuries (China, Japan, Canada) have been pulling back for years. ARK Invest found that the share of Treasuries held by the largest foreign creditors dropped from 23% to just over 6% in the past 13 years. The Fed is STILL running down its balance sheet. So who's going to buy all this debt? Washington's answer: stablecoin issuers. Treasury Secretary Bessent said it himself: "A thriving stablecoin ecosystem will drive demand from the private sector for US Treasuries and help rein in the national debt."Think about what that actually means. The government is counting on a $315 billion crypto product (run largely by a company in El Salvador that just got its first real audit last week) to help finance a $1.9 TRILLION annual deficit. Stablecoin issuers currently hold less than 2% of outstanding Treasury bills. Even if the market hits $2 trillion by 2028 like Standard Chartered projects, that's still just a rounding error against $39 trillion in total debt. This is literally a NARRATIVE designed to make the debt problem sound manageable.But the Federal Reserve published a study showing that for every $1 that moves from bank deposits into stablecoins, bank lending contracts by roughly 50 cents. Stablecoin issuers can't make loans. The GENIUS Act prohibits it. They can ONLY hold Treasuries, reverse repos, and cash equivalents.So when deposits leave banks and flow into stablecoins, that money stops funding mortgages, small business loans, and commercial credit. It starts funding government debt instead.The US Treasury itself estimated stablecoins could drain up to $6.6 TRILLION from the banking system.That's not "strengthening the dollar." That's redirecting the lifeblood of the real economy into government IOUs while starving Main Street of credit.And then there's the run risk nobody wants to discuss.Fed Governor Michael Barr said it yesterday:Stablecoin issuers have every incentive to chase higher returns on their reserves. But unlike banks, they CANNOT access the Fed's discount window. If a stablecoin run happens, issuers dump Treasuries into the market all at once.Stablecoin inflows push Treasury yields down 2-2.5 basis points. Outflows spike yields UP 6-8 basis points. Easy in. Ugly out.Meanwhile, Tether is the 800-pound gorilla. $185 billion in circulation. 550 million users. And until last week, it had never had a Big Four audit. It just hired KPMG after 12 years of operating with nothing but quarterly attestations.This is the entity Wall Street is celebrating as the future of dollar dominance. A company headquartered in El Salvador that fought transparency in court twice and LOST both times.Here's what Solomon and Mnuchin are actually telling you if you listen carefully:Stablecoins create captive demand for short-term US government debt. Foreign governments don't want to hold Treasuries anymore. So Washington's solution is to get 550 million retail users in emerging markets to hold them instead through a digital wrapper called a "stablecoin."The holders get zero interest. The GENIUS Act explicitly prohibits it. The issuers pocket the Treasury returns. Tether made $10 billion in profit last year. And the real economy loses credit while the government gets cheaper funding.This is a classic Wall Street pitch to sell financial innovation as progress:"This strengthens the system. This is good for everyone."Then the leverage builds, the risks concentrate, and the people who sold you on it are nowhere to be found when it unwinds.Stablecoins are NOT saving the dollar. They're a $315 billion shadow money market fund with no Fed backstop, no deposit insurance, and run dynamics that could destabilize the very Treasury market they're supposed to support.If you want to hold dollars, hold dollars. If you want to own the asset that central banks are actually buying instead of Treasuries, you already know what that is...🥇 This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1m 23s | ||||||

| 4/1/26 |  The World post Feb 28 | Craig Shapiro | 1. Strategic Actions and Decisions* Shift to a more conservative portfolio posture: Reduce exposure to risk assets, particularly high-valuation tech, as the market is likely in the early stages of repricing for a slower-growth, higher-inflation reality. [00:02:30]* Rotate capital into hard assets and domestic infrastructure: Focus on U.S. energy producers, petrochemical companies benefiting from cheap natural gas, and domestic AI infrastructure plays, which are supported by the “America First” policy shift. [00:21:15]* Increase gold allocations as a strategic hedge: Treat gold not just as a short-term trade but as a core portfolio component to protect against dollar hegemony risks and the failure of bonds as a safe-haven asset. [00:23:50]* Implement hedges using volatility: Use volatility as an asset class to hedge portfolios, as traditional hedges like long-duration bonds may not provide the expected protection in this environment. [00:26:20]* Avoid speculative assets and “Momentum Bro” trades: Exit or short highly speculative assets (e.g., Shitcos, ARK-like strategies) as the liquidity and risk-on conditions that fueled them are no longer present. [00:36:30]2. Executive SummaryThe market is facing a regime shift driven by the closure of the Strait of Hormuz, leading to a sustained period of slower global growth, higher energy costs, and elevated inflation. The administration’s pullback from global conflict suggests a new, isolationist “America First” economic playbook focused on domestic manufacturing. This environment invalidates previous investment strategies. Investors should rotate from overvalued tech into U.S. energy, infrastructure, and gold, while using volatility as a hedge. The Fed’s ability to rescue markets is hampered by inflation, and a significant correction in risk assets is likely before any meaningful policy response is triggered.3. Key Takeaways and Practical Lessons1. Market Regime Change is Underway, Not a Transitory Event: The closure of the Strait of Hormuz represents a fundamental shift in global trade and energy security, moving the market from a “geopolitical risk premium” to a “new economic reality” of structurally higher costs.* Practical lesson: Re-evaluate long-term models that assumed open trade routes and stable energy prices; re-run valuations under a scenario of sustained $70-90 WTI and higher term premiums.2. The Old “Fed Put” is Broken: The Fed’s ability to bail out markets is constrained by sticky inflation and high energy prices; they will likely be late to cut rates, making a growth-driven recession more painful for stocks.* Practical lesson: Do not buy the dip expecting an immediate Fed response. Deploy capital only after a significant (25-30%) market correction, which would be the trigger for potential Fed intervention.3. Long-End Bonds are Not a Safe Haven: With rising deficits, a massive corporate capex call on capital, and global central banks diversifying away from Treasuries, the long bond is a source of risk, not a portfolio stabilizer.* Practical lesson: Replace long-duration Treasuries in a portfolio with a steepener trade (short long-end) or allocate that capital to gold, which benefits directly from dollar debasement concerns.4. The AI Boom is Morphing from a Tailwind to a Headwind: The transition from internally funded AI CapEx to debt-financed spending is crowding out the broader economy, while AI-driven labor displacement is a looming credit risk for white-collar employment and banking.* Practical lesson: Focus on AI enablers (semis, energy) that provide the “picks and shovels,” but reduce exposure to overvalued software names that face margin pressure from higher capital costs and potential demand destruction.5. Speculation is Entering a Death Phase: The environment of tight liquidity and rising risk-free rates is ending the era of speculative assets (meme stocks, shitcoins). The marginal buyer for these assets has evaporated.* Practical lesson: Close out long positions in high-beta, unprofitable “story” stocks. The trading dynamic will shift from chasing returns to capital preservation, making volatility selling strategies increasingly dangerous.Follow Craig here on X - @ces921 Watch on youtube below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 44m 42s | ||||||

| 3/30/26 |  Wall Street is rewriting the rules of the S&P 500 | And that not to protect your retirement.But to fast-track trillion-dollar money-losing AI companies into your portfolio.Let me explain what's about to happen.SpaceX, OpenAI, and Anthropic are all preparing to go public THIS YEAR.Combined expected market cap: roughly $3 TRILLION.SpaceX is targeting a June IPO at a $1.5-1.75 trillion valuation. It merged with xAI in February and plans to raise up to $50 billion - the largest IPO in American history.OpenAI is targeting Q4 2026. It just raised $110 billion at a $730 billion valuation from Amazon, SoftBank, and Nvidia. It projects a $14 billion LOSS this year. It doesn't expect to turn a profit until 2029 or 2030. It trades at 65 times revenue.Anthropic is valued at $380 billion. Also expected to list this year.Now here's where it gets dangerous for passive investors:From 2016 to 2025, the ENTIRE US IPO market raised $469 billion total. These 3 companies alone want to raise more than that in a single year.But it gets WORSE.S&P Dow Jones, Nasdaq, and FTSE Russell are ALL considering fast-track rules that would shove these companies into major indexes within DAYS of going public - bypassing the standard 12 month seasoning period.Roughly $24 trillion in passive funds is tied to the S&P 500 alone. Those funds MUST buy whatever gets added.So a company like OpenAI that's burning $14 billion a year, valued at 65x revenue, with no path to profitability for four years could become a mandatory holding in your 401k before it even reports a single quarterly earnings as a public company.Nasdaq is proposing a "Fast Entry" rule: inclusion after just 15 trading days. SpaceX reportedly made early index inclusion a CONDITION of choosing Nasdaq over the NYSE.The inmates are running the asylum.Index providers aren't rewriting rules because these companies earned their place. They're rewriting rules because SpaceX is too big to ignore and too lucrative to lose to a competing exchange.If all 10 of the largest venture-backed companies go public and get fast-tracked, their combined weight could reach 4.5% of the S&P 500 - more than the ENTIRE energy sector.Think about that.Companies that collectively lose billions per year could outweigh every oil and gas producer in America inside the most important retirement index on Earth.This is the passive indexation trap I've been warning about.You don't get to choose. You don't get to vote. The index committee decides, the ETFs execute, and your retirement savings follow orders.When the index is being engineered to absorb trillion-dollar speculative bets, the smartest move is to stop blindly following it.Own what you understand. Own what makes money. Own what's priced for reality, not fantasy.GOT GOLD? This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 0m 51s | ||||||

| 3/30/26 |  Michael Howell | The Liquidity King | The Tide is Going Out. | 1. Strategic Actions and Decisions* Execute a Rotation into Energy and Defensive Staples: Capital should be moved out of early-cycle technology and financial sectors into late-cycle assets, specifically integrated energy, resources, and consumer staples. [00:10:25]* Monitor the Liquidity Cycle for a 2027 Bottom: Portfolio strategy should be framed around a structural decline in global liquidity that is expected to reach its cyclical low point in 2027. [00:43:03]* Hedge Against Monetary Inflation with Gold: Exposure to gold should be maintained as a hedge against currency debasement, with the People’s Bank of China (PBoC) injections serving as the primary marginal price driver. [00:50:03]* Acquire Agriculture Positions via the DBA ETF: The agriculture sector is identified as a primary “catch-up” trade within the commodity complex, targeting a price level of approximately $31. [01:32:04]* Transition from Cap-Weighted to Equal-Weighted Indices: High concentration risk in the “Magnificent Seven” and SPY warrants a move to the RSP (Equal-Weight S&P 500) to avoid unprecedented technical exhaustion signals. [01:37:18]2. Executive SummaryThe global liquidity cycle has peaked, triggering a defensive shift into 2026 as capital is siphoned into the real economy to fund rising energy costs and government deficits. Michael Howell identifies a “refinancing trap” where exponential global debt outpaces cyclical balance sheet capacity, while Rick Bensinger highlights rare technical exhaustion in market-cap-weighted indices. With the People’s Bank of China aggressively devaluing the yuan against gold and the Fed sidelined by persistent inflation, the panel projects a structural bear market bottoming in 2027. Leadership must prioritize capital preservation through tangible commodities and defensive value sectors.3.Key Takeaways and Practical Lessons1. The Debt-Liquidity Mismatch: Financial crises are triggered when the exponential growth of global debt outpaces the cyclical capacity of financial balance sheets to refinance that debt.* Practical Lesson: Audit the “refinancing risk” of all holdings; prioritize firms with robust internal cash flows that do not rely on constant debt rollovers to survive tightening cycles.2. Bond Volatility Acts as a Credit Constraint: A volatile bond market forces dealer banks to increase “haircuts” on collateral, which effectively reduces the total amount of credit available to the global system.* Practical Lesson: Monitor the Move Index as a primary early-warning system; if bond volatility remains elevated, keep equity exposure defensive regardless of positive media sentiment.3. Real Economy “Liquidity Tax”: Capital diverted to fund rising energy prices, working capital, and government spending is directly subtracted from the liquidity available for financial assets.* Practical Lesson: Treat energy price spikes as a signal to reduce valuation multiples for tech holdings, as rising real-world costs inevitably drain the liquidity available for growth stocks.4. China as the Strategic Gold Driver: The People’s Bank of China is aggressively injecting liquidity and devaluing the yuan against gold to manage its internal debt-deflation crisis.* Practical Lesson: Monitor yuan-denominated gold prices to gauge global demand floors, as Chinese central bank activity is now a more significant marginal driver than Western retail trends.5. Technical Concentration Exhaustion: Rare technical exhaustion signals in the “Magnificent Seven” and broad cap-weighted indices suggest the “momentum trade” has reached a terminal phase.* Practical Lesson: Reduce reliance on passive cap-weighted ETFs and transition to equal-weighted alternatives or specific commodity ETFs like Agriculture (DBA) for late-cycle protection.Follow Michael Howell On X here - @crossbordercap Watch on Youtube Down Below - This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 1h 41m 58s | ||||||

| 3/27/26 |  Live with George Noble | This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit georgenoble.substack.com/subscribe | 5m 40s | ||||||