Estimating Future Discretionary Benefits Without Monte Carlo Simulation

From Finance Tech Brief By HackerNoon by HackerNoon

February 13, 2026 · 12 min

About this episode

This episode discusses a deterministic framework for estimating future discretionary benefits in life insurance without relying on Monte Carlo simulations.

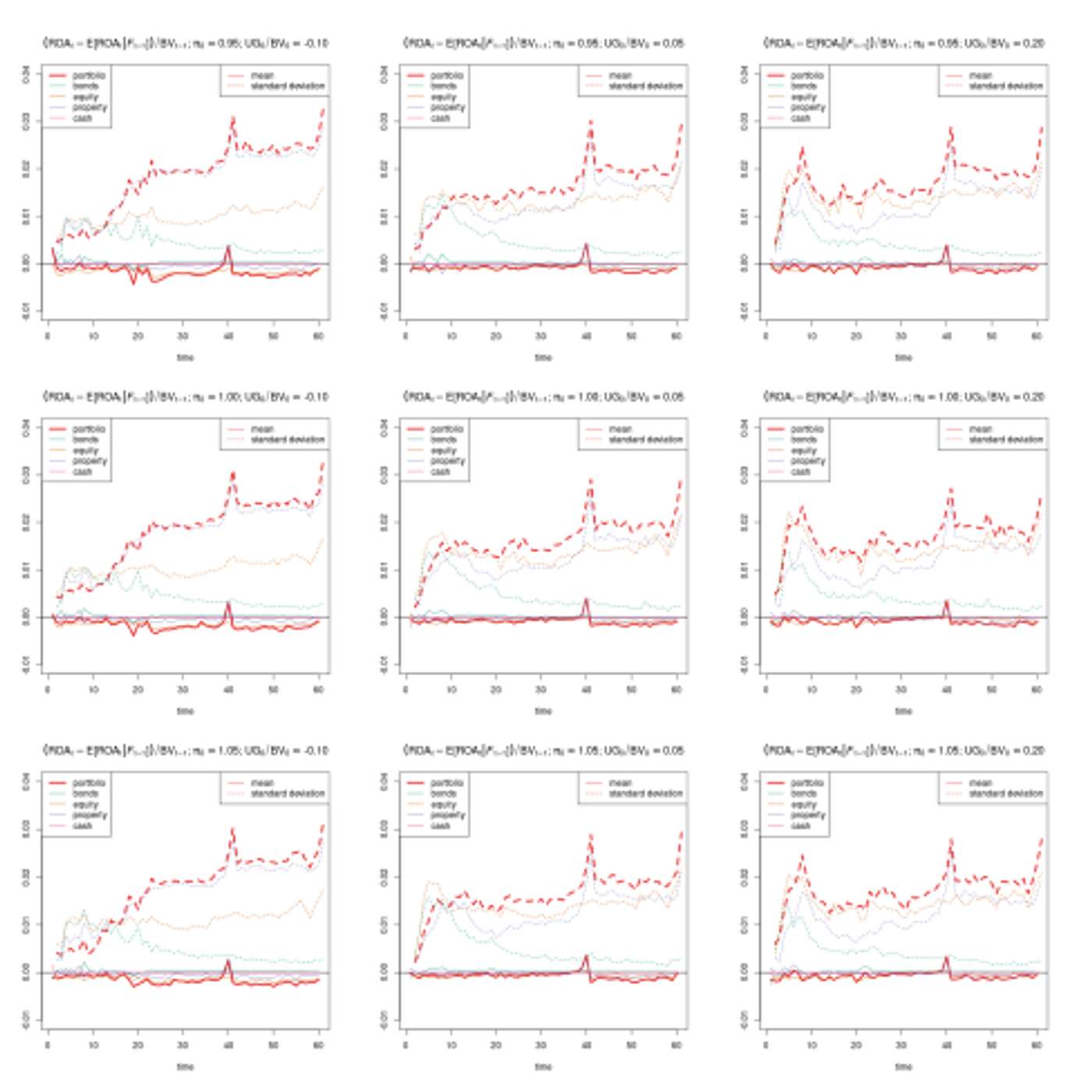

This story was originally published on HackerNoon at: https://hackernoon.com/estimating-future-discretionary-benefits-without-monte-carlo-simulation . A deterministic framework for estimating future discretionary benefits in life insurance, offering tight bounds without Monte Carlo simulation. Check more stories related to finance at: https://hackernoon.com/c/finance . You can also check exclusive content about #insurance-regulation , #market-consistent-valuation , #solvency-ii , #actuarial-modeling , #mean-field-libor-market-model , #asset-liability-management , #monte-carlo-valuation , #financial-risk-modeling , and more. This story was written by: @solvency . Learn more about this writer by checking @solvency's about page, and for more stories, please visit hackernoon.com . This article presents a deterministic method for estimating future discretionary benefits in life insurance portfolios by deriving stable upper and lower bounds, avoiding reliance on Monte Carlo simulations while maintaining market consistency.

Topics covered

- life insurance

- discretionary benefits

- Monte Carlo simulation

- financial modeling

- actuarial science

Keywords

- discretionary benefits

- life insurance

- Monte Carlo simulation

- financial risk modeling

- actuarial modeling

Mentioned in this episode

Organizations: HackerNoon

More episodes of Finance Tech Brief By HackerNoon

- The Fintech Infrastructure Gap That's Quietly Choking a $454 Billion Industry · June 12, 2026 · 7 min

- A Voucher Is Not a Payment - Most Platforms Disagree · June 11, 2026 · 6 min

- Grandma’s Retirement Money, Grok, and 100,000 AI Brains · June 11, 2026 · 8 min

- 297 Blog Posts To Learn About Money · June 8, 2026 · 1h 11m

- Designing Global Electronic Bank Statement Frameworks Across 25 Plus Countries · June 2, 2026 · 7 min

- Programmable payment Recovery in Failing Networks · June 2, 2026 · 8 min

Explore listener stats, chart rankings, contacts and more on the Finance Tech Brief By HackerNoon podcast page.